Another Victory: Successfully Defending a Large Crypto Trader Against Income Tax Notice India 2026

Successfully Defending a Large Crypto Trader Against Income Tax Notice - India 2026

In recent years, the Income Tax Department (ITD) has increased scrutiny on cryptocurrency (Virtual Digital Assets or VDA) transactions due to concerns about tax evasion and underreporting. Many traders and investors have faced tax notices questioning their crypto income, leading to lengthy compliance processes.

This article explores the case of one of our clients, a high-volume crypto trader who received multiple tax notices but we successfully defended his income declaration, resulting in a favourable assessment order under Section 143(3) of the Income Tax Act, 1961. In this article, we analyze the key legal strategies that helped him avoid additional tax liabilities.

Table of Contents

Introduction

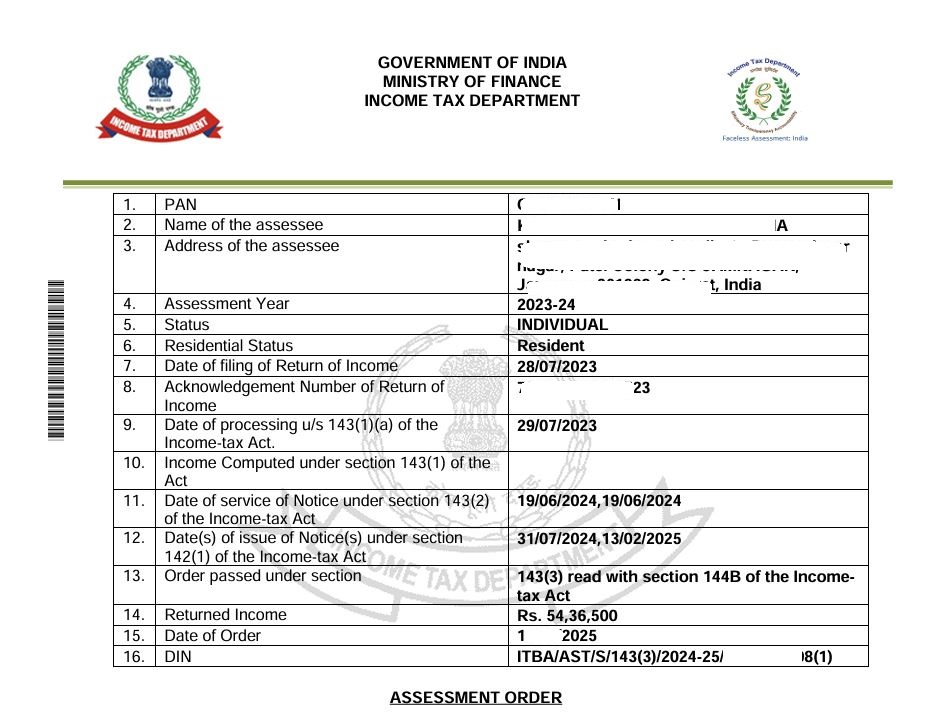

In the intricate and often daunting landscape of Indian income tax assessments, this is a case study of procedural integrity, and a favourable outcome achieved through transparent disclosures and responsive communication. For the Assessment Year 2023–24, Our client’s tax affairs underwent a detailed scrutiny by the Income Tax Department, especially concerning his involvement in trading Virtual Digital Assets (VDAs), commonly referred to as cryptocurrencies. Despite this potentially complex area of financial activity, our client - Mr. KM emerged unscathed, with Income tax Assessing Officer accepting the declared income in full.

Background of the Case

- Initial ITR Filing & Selection for Scrutiny

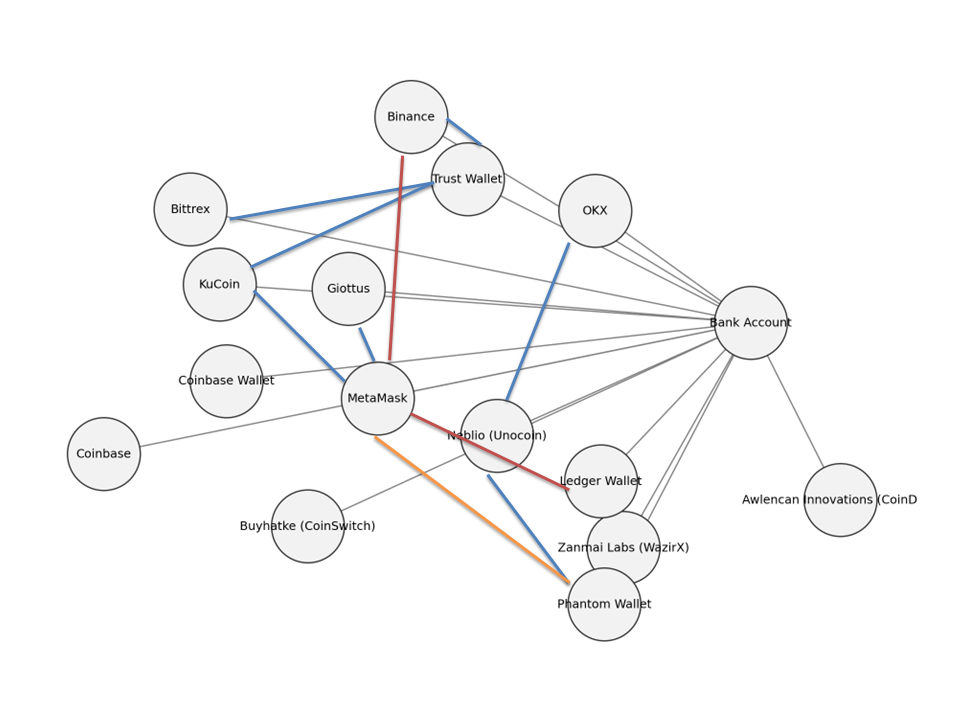

The client had engaged in arbitrage trading, day and swing trading, which involved numerous high-value transactions across various international and Indian crypto exchanges. He was also using various crypto wallets such as MetaMask, Phantom and hardware wallet.

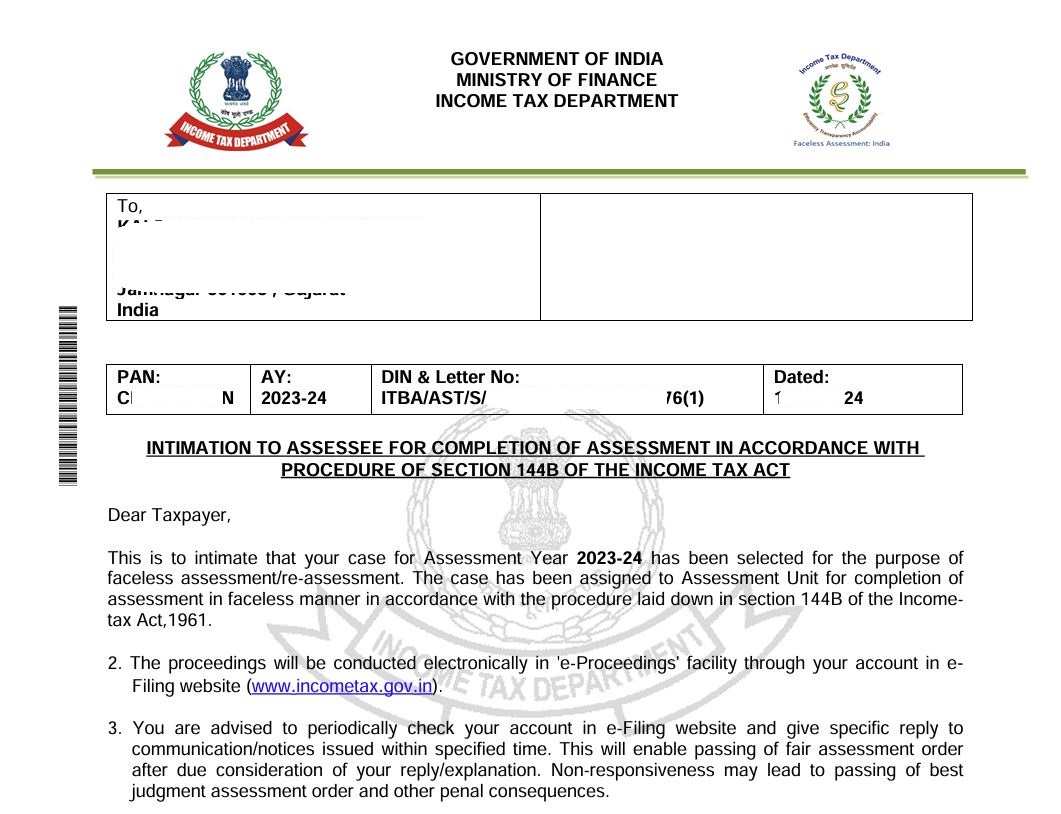

He had filed his Income Tax Return (ITR) for AY 2023-24 before tax filing due date, declaring a total income of ₹54,36,500. The return was processed under Section 143(1) the very next day, on July 29, 2023. However, the ordeal did not end there. On June 19, 2024, the client received an Intimation under Section 144B of the Income Tax Act, 1961, notifying him that his case was selected for scrutiny.

- His case was selected for scrutiny because:

- He had substantial transactions in Virtual Digital Assets (VDA). the red flag was raised over significant receipts from Virtual Digital Asset transfers.

- The income reported from crypto trading appeared substantially low relative to transaction volumes.

- He had substantial foreign assets and was the Owner (UBO - ultimate beneficial owner of multiple companies overseas)

- The ITD wanted to verify the source of investment, capital gains, and losses claimed.

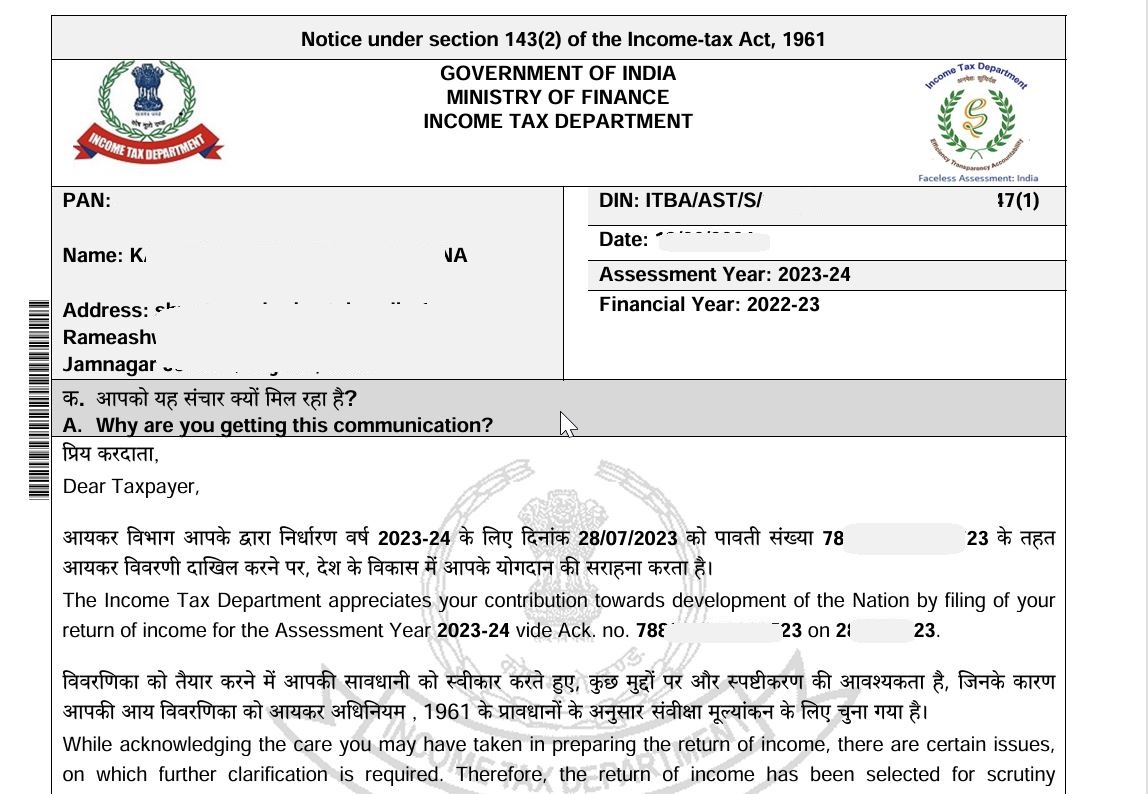

Simultaneously, a Notice under Section 143(2) was issued on the same date, 19 June 2024, asking him to provide explanations and documentation supporting the claims in his return. This triggered the start of the official assessment proceedings.

- Initial Notices Issued by the Income Tax Department

The client received the following notices:

- Intimation under Section 144B - An Intimation under Section 144B of the Income Tax Act, 1961 informs the taxpayer that their case has been selected for faceless assessment or reassessment. It marks the beginning of proceedings that will be conducted electronically, without any physical interface, in accordance with the faceless assessment scheme introduced to ensure greater transparency, efficiency, and accountability in tax administration.

- Notice under Section 143(2) - A Notice under Section 143(2) of the Income Tax Act, 1961 is issued when the Income Tax Department selects a taxpayer’s return for scrutiny assessment. It indicates that the department requires further information or clarification on certain aspects of the return to verify its correctness and completeness. The notice allows the taxpayer an opportunity to support their return with relevant documents and explanations.

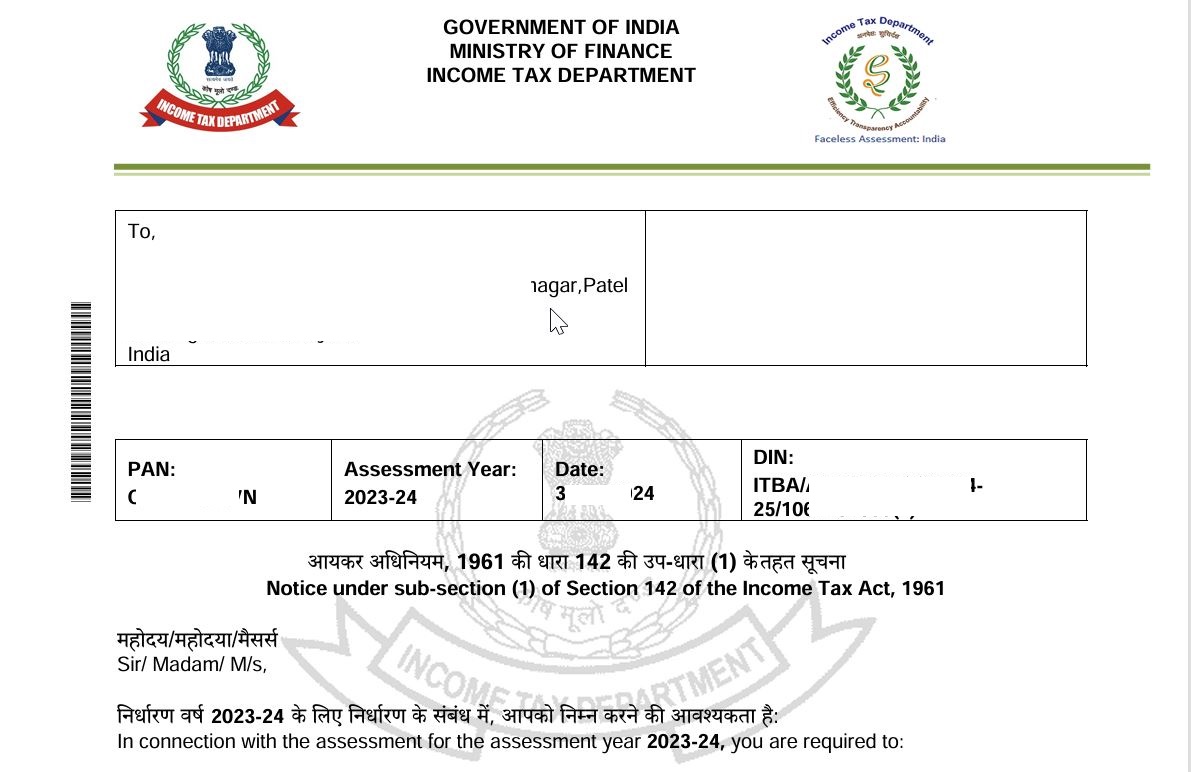

- Notice under Section 142(1)– A Notice under Section 142(1) of the Income Tax Act, 1961 is issued by the Income Tax Department to request additional information, documents, or accounts from the taxpayer to assist in completing the assessment. It may also ask the taxpayer to appear or respond to specific queries about their return. Compliance with this notice is mandatory and helps the assessing officer determine the accuracy of the filed return. In this particular case, Department sought additional documents and explanations.

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India.

- Scrutiny Intensified: Notice Under Section 142(1)

Subsequently, a Notice under Section 142(1) dated July 31, 2024, demanded detailed documentation and explanations. The annexure attached to the notice sought comprehensive records, including:

- A business profile of various entities from FY 2018–19 till date segregated year wise.

- Profit & Loss account, Balance Sheet, and Tax Audit Report from FY 2018–19 till date.

- Computation of total income and.

- Detailed bank statements with interest and balances.

- Bank Statements, Books of Accounts, Profit & Loss account & Balance Sheet of overseas entities.

- Specific breakdown of Virtual Digital Asset transactions, including reconciliation between various Crypto Exchanges, Blockchain Wallets, Bank statements, Form 26AS (which records TDS and reported income) and the figures reported in ITR of the client.

The department had noted cryptocurrency transactions across various Indian and international platforms such as Binance, Coinbase, KuCoin, OKX and Bittrex. Indian exchanges mentioned included:

- Awlencan Innovations India Limited

- Buyhatke Internet Private Limited

- Giottus Technologies Private Limited

- Neblio Technologies Private Limited

- Zanmai Labs Private Limited

Further, the AO sought details of all transactions from the blockchain wallets - MetaMask, Trust Wallet, Coinbase Wallet, Phantom Wallet & Hardware Ledger wallet. The AO sought a critical review of the source of funds, volume of trading, reconciliation with TDS details, and any unreported capital gains.

Our Approach

Our team undertook the massive task of compiling accounts for Virtual Digital Asset (VDA) transactions spanning multiple platforms — including Indian and international crypto exchanges, blockchain wallets and Bank statements. This was an exhaustive and high-stakes exercise, particularly in light of Income Tax department’s stringent requirements. Below is a comprehensive step-by-step guide our team had taken to comply with accounting, reconciliation, tax compliance, and financial reporting related to VDAs. Its given here only for reference purpose.

🔍 Steps taken to prepare accounts for VDA Transactions

📁 Step 1: Collated Data from All Platforms

1.1 International Crypto Exchanges

Platforms: Binance, Coinbase, KuCoin, OKX, Bittrex

- Download complete transaction history (trades, deposits, withdrawals, staking rewards, fees).

- Ensure you include spot trades, futures, P2P transactions, and margin trades.

- Export data in CSV or Excel formats for compatibility with reconciliation tools.

1.2 Indian Crypto Exchanges

Platforms: Awlencan Innovations (possibly CoinDCX), Buyhatke (possibly CoinSwitch), Giottus, Neblio (Unocoin), Zanmai Labs (WazirX)

- Collect complete trade reports, ledger summaries, P2P transactions.

- Note timestamps, INR transaction values, and GST or TDS deductions (if any).

1.3 Blockchain Wallets

Wallets: MetaMask, Trust Wallet, Coinbase Wallet, Phantom Wallet, Hardware Ledger

- Exported transaction logs using blockchain explorers like Etherscan, Solscan, or BSCScan.

- Recorded details for each wallet:

- Token type

- Date/time

- Wallet address (public)

- Gas fees

- Transaction hash

- For hardware wallets, our team used integration tools to extract transaction reports.

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India.

🔎 Step 2: Identified and Tagged All Transactions

- Categorized transactions:

- Buy/Sell trades

- Swaps/DEX trades

- Transfers (between own wallets/exchanges)

- Airdrops

- Staking income/interest

- NFT trades (if applicable)

🧾 Step 3: Bank Statement Reconciliations done - Matched bank statement entries (deposits to exchanges, withdrawals, INR settlements) with:

- Crypto buy/sell transactions

- Fiat gateway providers

Our team ensured that

- Deposits from personal vs. business accounts are clearly segregated

- UTR/reference IDs match with exchange ledger IDs

🧮 Step 4: Cross-Platform Reconciliations prepared

4.1 Inter-Wallet Transfers

- Matched blockchain wallet "sent" transactions to exchange "deposit" entries (or vice versa).

- Confirmed consistency via:

- Wallet addresses

- Token amount

- Transaction hash

4.2 Inter-Exchange Transfers

- Used timestamp & hash to confirm that:

- Outbound from Exchange A = Inbound on Exchange B

- Any missing tokens were investigated along with client (stuck transactions, delisted tokens)

📊 Step 5: Trading Volume Analysis

- Computed:

- Total INR spent on purchases

- Total INR received from sales

- Net holding value as of balance sheet date

- Highlighted all:

- High-frequency trading

- Arbitrage movements

- DeFi exposure

🧮 Step 6: Capital Gains Computation (as per Indian tax laws)

- Applied FIFO (First-In, First-Out) method

- Report INR equivalent of gains using conversion rate on transaction date

📑 Step 7: Reconciled with TDS Reports (Form 26AS & AIS)

- Downloaded Form 26AS and AIS from Income Tax portal

- Checked:

- TDS entries under Section 194S for crypto trades (especially P2P and exchange trades above threshold)

- TDS deducted by platforms like WazirX, CoinDCX, CoinSwitch

- Matched TDS entries with:

- Corresponding sell transactions

- Wallet addresses and exchange reports

- Identified and prepared detailed explanations for :

- Under-reported trades

- Mismatch in TDS vs. reported amount

🧮 Step 8: Source of Funds Analysis

- Traced initial INR capital:

- Matched personal bank account funding

- Detailed Explanations provided for the following:

- Alleged disproportionate trading volume vs. known income

- Funds from third-party accounts without documentation

- Use of foreign remittances (FEMA/ODI norms)

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India.

🧾 Step 9: Unreported Capital Gains

- Cross-verified exchange and wallet data with past tax returns to ensure that there was no unreported capital gains in any of the financial years.

🧯 Step 10: Final Financial & Tax Reporting

10.1 Prepared Crypto Accounts Ledger

- Created a detailed digital asset register:

- Date

- Token

- Quantity

- Buy/Sell rate in INR

- Exchange/wallet used

- Fees

- Capital gains computed

10.2 Disclosure made in the Financials submitted

- Showed VDA holdings as assets under foreign assets schedule – Sch FA.

- Disclose trading/income in Schedule VDA

- Audited financial statements: Profit & Loss account and Balance Sheet

Our team explained the apparent discrepancies between high-volume crypto activity and modest capital gains by detailing the nature of his trading and statements stated above. All these were properly documented under Schedule VDA, Schedule FA, Schedule AL in our responses, as per the new reporting requirements introduced by the Income Tax Act from FY 2022–23.

Final Investigation and Resolution

To leave no stone unturned, the Income Tax Department issued a second 142(1) notice on February 13, 2025, seeking additional clarifications about crypto transactions and specific purchases, including a high value luxury car purchased by our client. We complied on behalf of our client and provided the following:

- Purchase invoice of the motor vehicle

- Bank transaction trail verifying the source of funds

- Reconciliation statements for VDA-related withdrawals that went into purchase of this high value luxury car.

The department reviewed all documents and found the disclosures to be comprehensive, accurate, and in line with the Income Tax provisions. There was no discrepancy found between the declared income and the substantiating evidence.

The Order Under Section 143(3): A Clean Chit

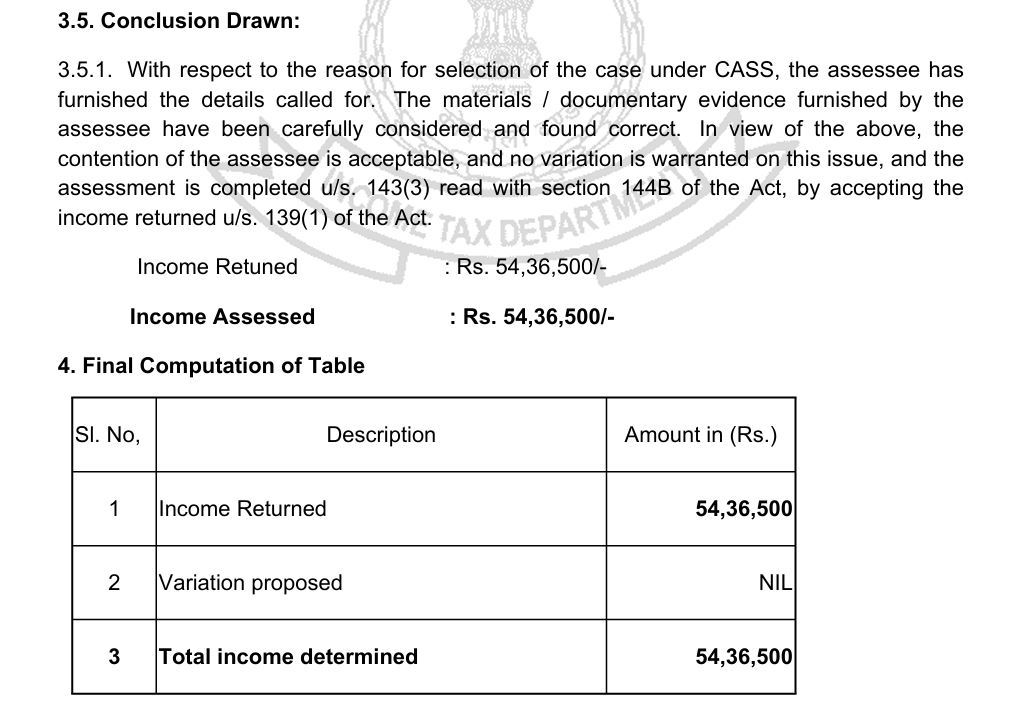

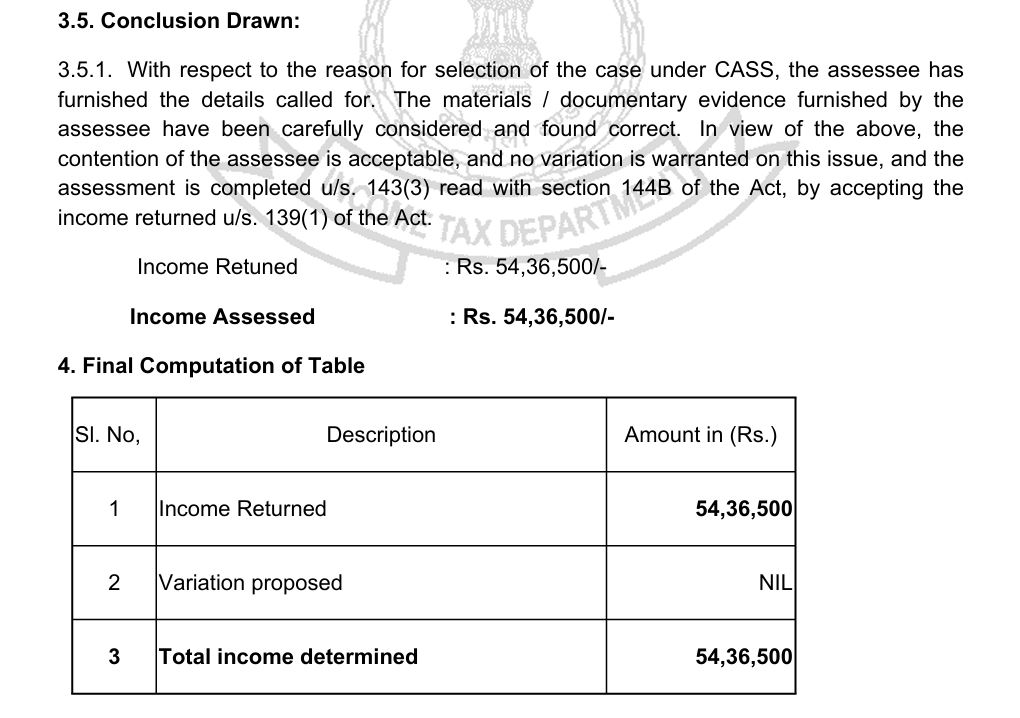

In May 2025, after lots of back and forth with the Assessing Officer on various clarifications sought by him, the Income Tax Department issued its final order under Section 143(3) read with Section 144B. The highlights of the order were:

- Returned Income: ₹54,36,500

- Assessed Income: ₹54,36,500

- Variation Proposed: NIL

This indicated that no additions, disallowances, or modifications were proposed by the Assessment Unit. The scrutiny was closed successfully without any tax demand, penalties, or further obligations.

The final assessment order emphasized that:

“The materials / documentary evidence furnished by the assessee have been carefully considered and found correct… no variation is warranted on this issue, and the assessment is completed u/s. 143(3) by accepting the income returned u/s. 139(1).”

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India.

Conclusion

This favourable outcome for our client was earned through diligent, meticulous effort, clarity, compliance, timely communication, and legal strategies employed by our firm. Here are key takeaways from this experience:

- Timely communication and Accurate Disclosure

All responses were filed within stipulated timelines, supported by meticulously prepared tables, visual charts, data flow diagrams, explanations, and complete Income tax schedules. These included Schedule VDA for crypto transactions, Schedule FA for foreign assets, and Schedule AL for asset-liability disclosures, ensuring accurateness in tax compliance reporting.

- Proper Documentation with detailed explanations

We created comprehensive documentation—covering both bank statements and cryptocurrencies exchanges and wallets — along with clear explanations for each transaction for the Assessing Officer, as outlined earlier. This streamlined the review process and facilitated a smoother understanding for the tax authorities.

A Case Study in Diligent Compliance

The number of income tax notices being issued have increased in recent years as Government cracks down on tax evaders and non tax filers. This is due to the fact that it has become common for people to hide their income, non payment of taxes, having high-value transactions, or filing defective returns. The journey of Client through the scrutiny maze is an exemplary case of how a taxpayer can navigate the challenges of a complex and evolving tax environment. Despite being flagged for high-volume crypto transactions — a segment under close watch by Indian tax authorities, we helped our client come unscathed because of preparedness, and clear communication.

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India.

DISCLAIMER

CMS Meta:

Comments