Managing and Responding to Income Tax Notices

Did you get an notice in mail from the Income Tax Department? If yes, do not worry and there is no need to get panic. We got your back. You can seek our Expert Assistance for Managing and Responding to Income Tax Notices service. We at CA Mitesh and Associates have a full-fledged team of experienced Chartered Accountants who can help you in replying to the income tax notice and further assist you as and when required.

Why did you receive an Income Tax Notice?

If the Income Tax Department is not satisfied with your particulars in the Income Tax Returns (ITR) or if they have a question/ doubt for you, they will send you a notice, letter or in serious cases even summon you.

If you filed your returns properly then you should not panic just because you got served a notice from the income tax department. Income Tax Department might have found certain discrepancies in data, errors in calculations, wrong entry of certain data, etc. In all such cases, the Income Tax Department issues a notice otherwise known as Intimation Order. Sometimes, even a minor error in tax return can cause you receive a notice from the tax department.

Further, considering the seriousness of income tax notice, it is prudent that you should consult a qualified Chartered Accountant who can look after your notice and guide you professionally as to how the same can be replied and resolved. Please do not try to resolve it yourself without professional guidance as it can come back to haunt you. Anything and everything that you provide to the department can be used against you so its better to consultant a qualified Chartered Accountant before responding.

How to Handle an Income Tax Notice - Our Easy Process

To effectively manage an income tax notice, follow our easy process. Simply send us a copy of your notice via WhatsApp/Email and schedule an appointment with our team. Our experienced CA will carefully review your case and discuss the reasons for the notice and recommend a course of action.

Next, our team will gather all necessary data and documents and prepare a response to the income tax department. We'll provide you with a draft of the response for your review and approval. Once finalized, we'll submit the response to the Income Tax Department on your behalf. Trust us to handle your income tax notice efficiently and effectively.

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Documents required to reply to an Income Tax Notice

The Documents required vary with the type of Income Tax notice that is served to the taxpayer. The basic documents needed to reply to an income tax notice would be:

Legal Procedures for Income Tax Notice

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Checklist for Responding to Income Tax Notice

- After the intimation notice under Section 143 (1) is received of the Income Tax Act,1961 the taxpayer has to make a reply within 30 days from the date when the notice is served.

- If the taxpayer fails to respond within the time that is prescribed then the Income Tax Returns will be processed with the necessary adjustments without providing any opportunity to taxpayers.

- Once the notice is received then the taxpayer should cross-check the name, address, and PAN number, mentioned in the notice.

- Similarly, it is necessary to cross-check the assessment year that is mentioned and verify the e filing acknowledgment number.

- Revised returns can be filed only when the taxpayer has made mistake in the original ITR filing. When the taxpayer has opted to revise the return it has to be filed within 15 days.

- The rectification return can be filed only when the taxpayer has found any fault or error in the order that is sent by the Income Tax Department.

- On-Page 2 of the notice that is issued you can understand the reason for which the notice has been issued. It also shows the difference of the mentioned income in the returns that file and Form 16/16A/ 26AS.

- If the intimation notice demands the taxpayers to pay an additional tax amount i.e demand notice then it has to be treated as the notice of demand u/s 156.

- On receiving this notice of the demand the taxpayer has to respond within 30 days to avoid the !% of the interest per month from the 30 days expiry period and a penalty is also imposed by the assessing officer.

Types of Income Tax Notice

| Type of Notice | Description |

| Notice u/s 143(1) - Intimation | This is one of the most commonly received income tax notices. The income tax department sends this notice seeking a response to the errors/ incorrect claims/ inconsistencies in an income tax return that was filed. If an individual wants to revise the return after receiving this notice, it must be done within 15 days. Else, the tax return will be processed after making the necessary adjustments mentioned in the 143(1) tax notice. |

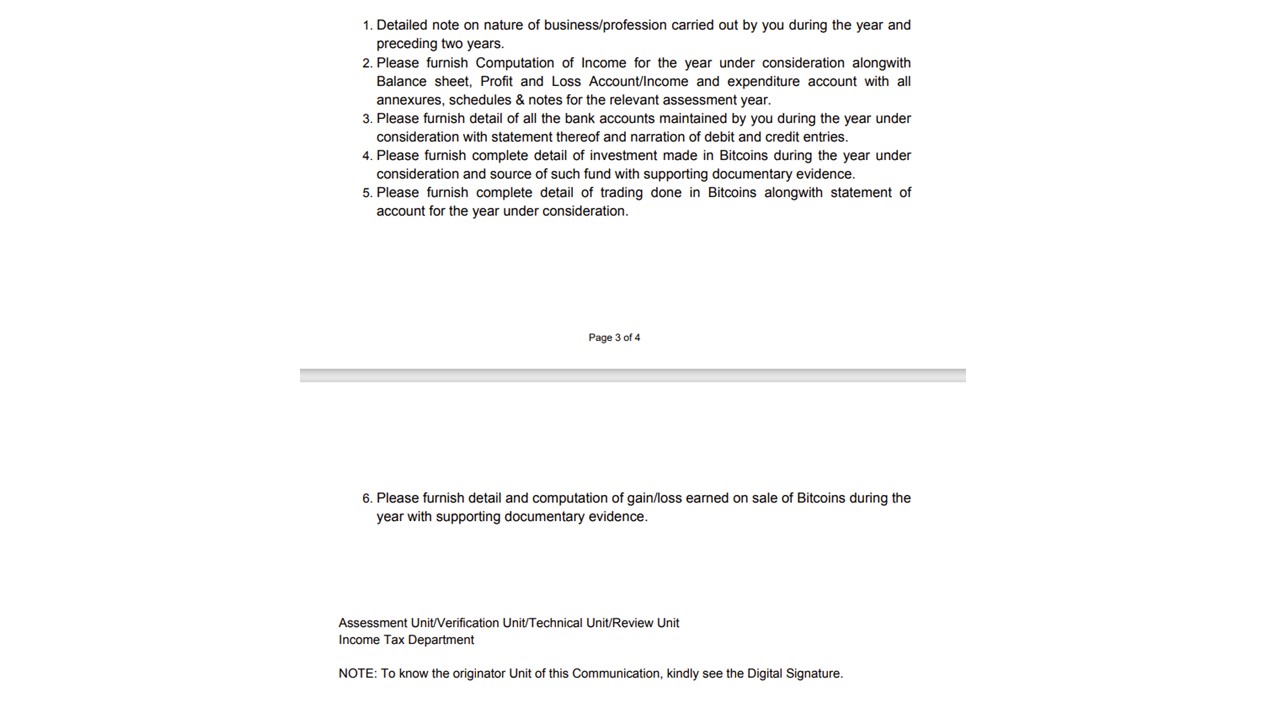

| Notice u/s 142(1) - Inquiry | This notice is addressed to the assessee when the return is already filed and further details and documents are required from the assessee to complete the process. This notice can also be sent to necessitate a taxpayer to provide additional documents and information. |

| Notice u/s 139(1) - Defective Return | An income tax notice under Section 139(1) would be issued if the income tax return filed does not contain all necessary information or incorrect information. |

| If tax notice under Section 139(1) is issued, you should rectify the defect in the return within 15 days. | |

| Notice u/s 143(2) - Scrutiny | An income tax notice under Section 143(2) is issued if the tax officer was not satisfied with the documents and information that was submitted by the taxpayer. Taxpayers who receive notice under Section 142(2) have been selected for detailed scrutiny by the Income Tax department and will have to submit additional information. |

| Notice u/s 156 - Demand Notice | This type of income tax notice is issued by the Income Tax Department when any tax, interest, fine, or any other sum is owed by the taxpayer. All demand tax notice will stipulate the sum which is outstanding and due from the taxpayer. |

| Notice Under Section 245 | If the officer has reason to believe that tax has not been paid for the previous years and he wants to set off the current year's refund against that demand, a notice u/s 245 can be issued. However, the adjustment of demand and refund could be done only if the individual has been provided proper notice and an opportunity to be heard. The recipient has to respond to the notice is 30 days from the day of receipt of the notice. If the individual does not respond within the specified timeline, the assessing officer can consider this as consent and proceed with the assessment. Therefore, it is advisable to respond to the notice at the earliest. |

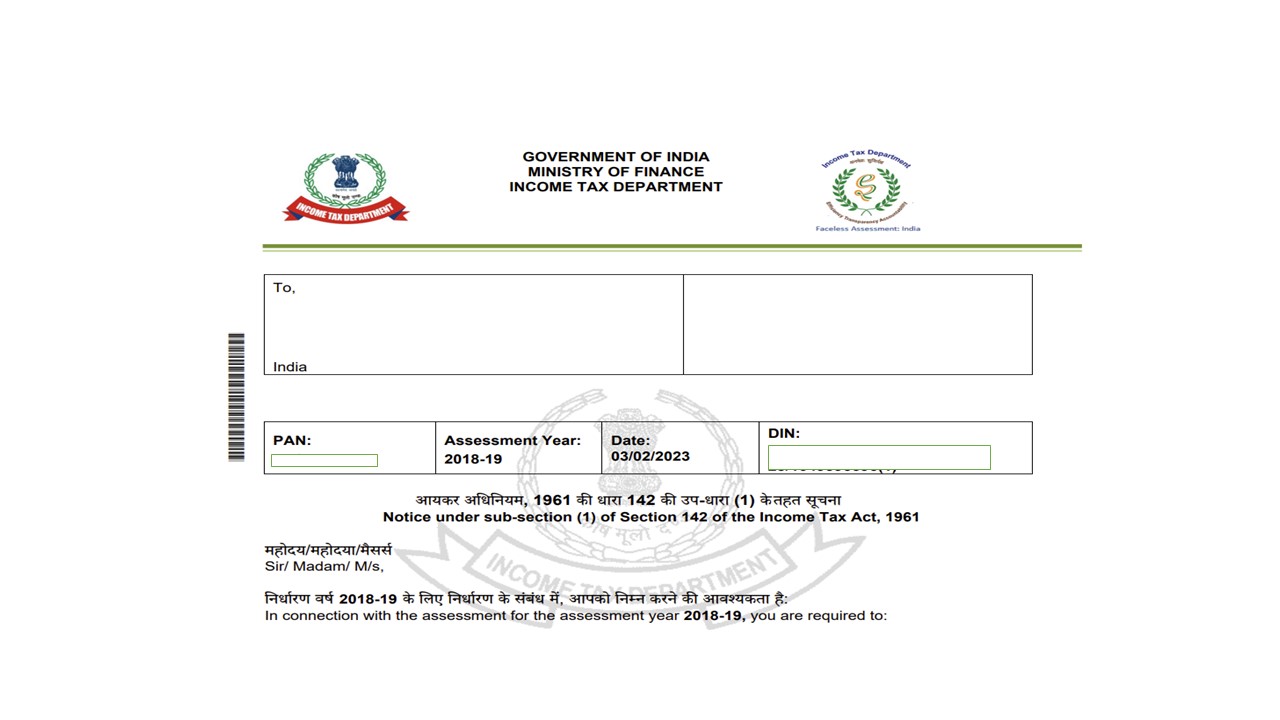

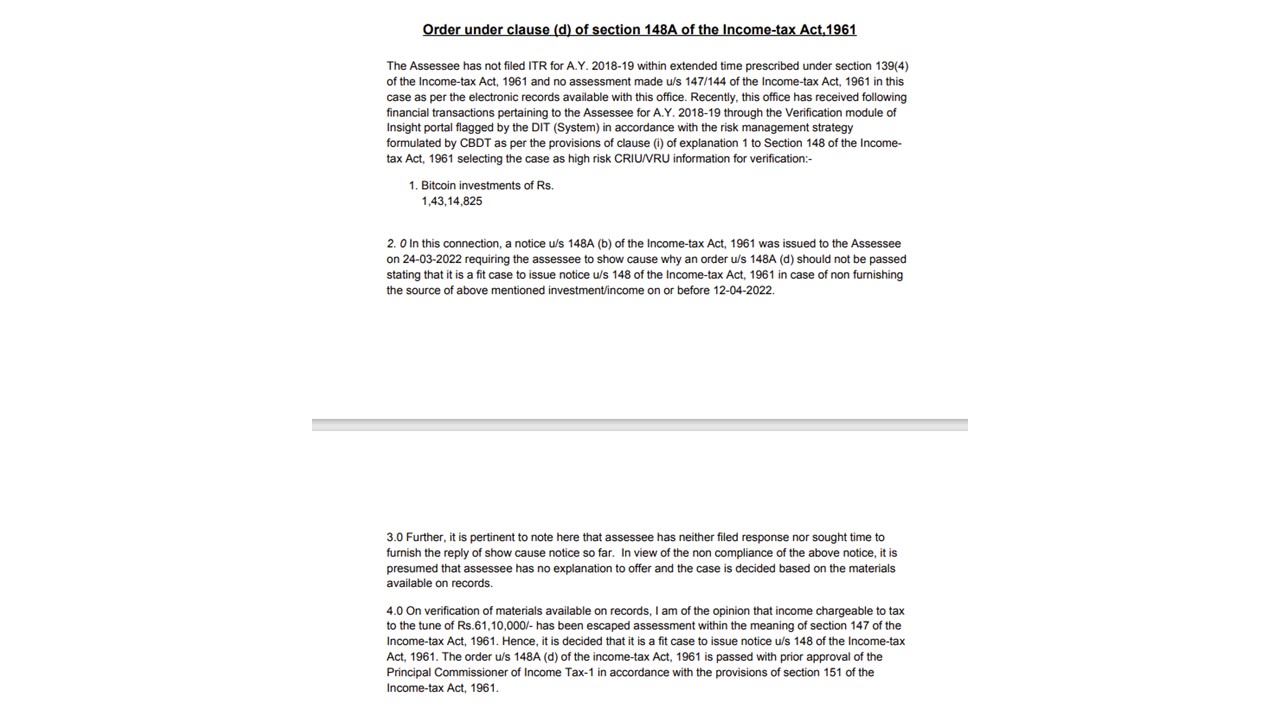

| Notice Under Section 148 | The officer may have a reason to believe that you have not disclosed your income correctly and therefore, you have paid lower taxes. Or the individual may not have filed his return at all, even if you must have filed it as per law. This is termed as income escaping assessment. Under these circumstances, the assessing officer is entitled to assess or reassess the income, according to the case. Before making such an assessment or reassessment, the assessing officer should serve a notice to the assessee asking him to furnish his return of income. The notice issued for this purpose is issued under the provisions of Section 148. |

It is important that as soon as you receive any notice from the Income Tax Department, you should be quick to understand its nature. We can help you ease the situation as we handle these things on daily basis along with our experience in years of practicing in taxation fields. Consequences of not complying with these notices can get you penalties and even imprisonment of various severities.

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

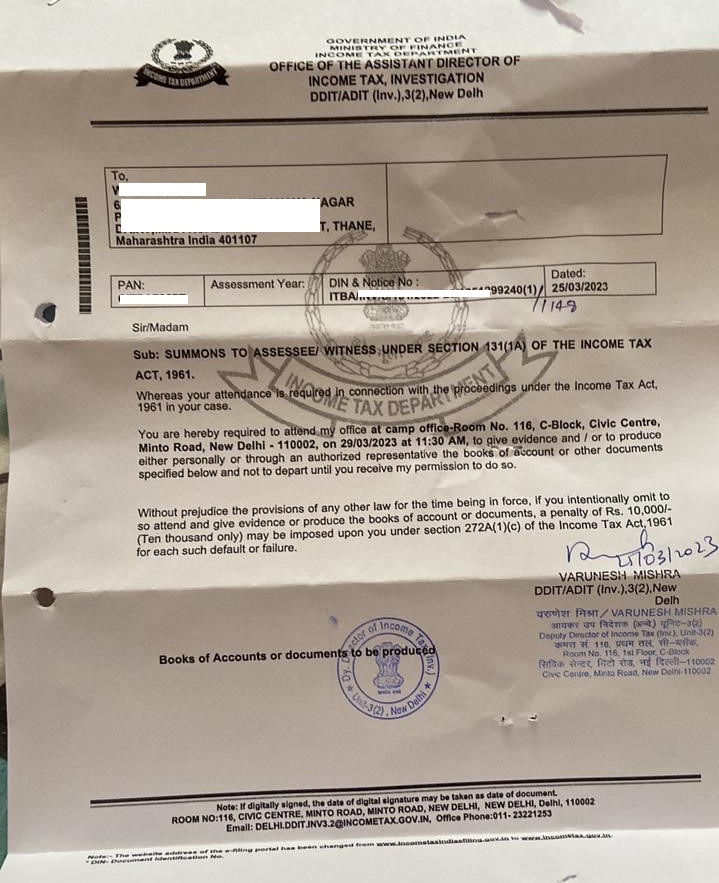

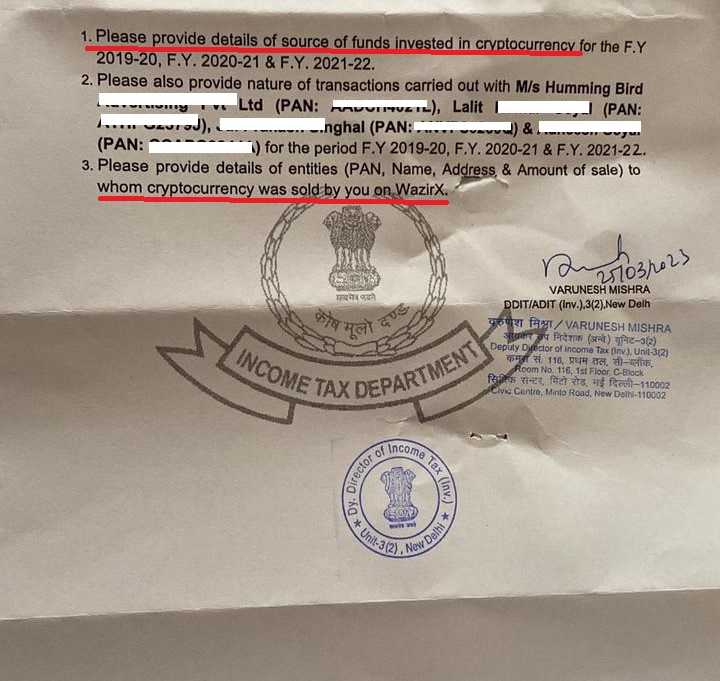

Sample Income Tax Notices that we have successfully defended

FAQs