Income Escaping Assessment 148 and 148A – Complete Guide & Step by Step Response

The Income Tax Department may initiate an Income Escaping Assessment under Sections 148 and 148A when taxpayers fail to report or include any specified income in their Income Tax Returns.

Table of Contents

- What is Assessment or Re-assessment?

- Issue of Notice Where Income Has Escaped Assessment Under Section 148

- Time Limit for Issuance of Notice Under Section 148

- Procedure to Be Followed Before Issuing Notice of Income Escaping Assessment Under Section 148A

- Time Limit for Passing an Order Under Section 148A

- Time Limit for Completion of Assessment by the Assessing Officer

- Circumstances When Income Is Deemed to Have Escaped Assessment

- Reasons to Believe

- Powers of AO to Assess Maximum Tax on Tax Evaders

- Prosecution Under Income Tax

- How to Respond to an Income Tax Notice Under Section 148A

- Sample Response Template for an Income Tax Notice Under Section 148A

Income Escaping Assessment

What is Assessment or Re-assessment?

Assessment or re-assessment refers to the process by which the department verifies and evaluates the accuracy of the income declared by the assessee and determines the correct tax liability. When the Assessing Officer (AO) has valid reasons to believe that taxable income has not been assessed or has been omitted for any assessment year, the AO is empowered—subject to the provisions of Sections 148 to 153—to assess or reassess that income. This authority also extends to any additional taxable income that may surface during the course of the re-assessment proceedings, even if it was not part of the initial trigger for reopening the case.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Issue of Notice Where Income Has Escaped Assessment Under Section 148

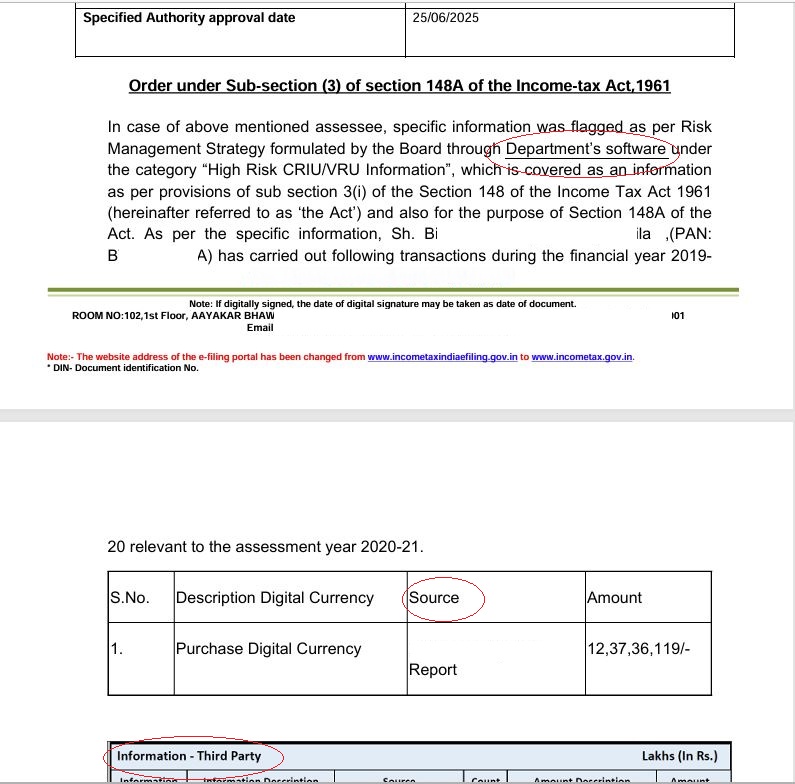

A notice under Section 148 can be issued only when specific conditions are satisfied. The AO must possess information indicating that taxable income has escaped assessment for the relevant assessment year, and before issuing the notice, the AO must obtain prior approval from the designated specified authority.

Information that may lead the AO to believe that income has escaped assessment includes:

Any data or alerts flagged under the Board-approved Risk Management Strategy for the relevant assessment year, which is the source of most notices issued to taxpayers.

Any audit objection pointing out that the assessment for that year was not carried out in accordance with the Income Tax Act.

Any information received under international agreements referenced in Section 90 or Section 90A.

Once satisfied that income has escaped assessment, the Assessing Officer will serve a notice under Section 148 requiring the taxpayer to file the return for the relevant assessment year. Additional notices may follow if the AO needs more documents or clarification to complete the assessment or re-assessment process.

Time Limit for Issuance of Notice Under Section 148

General Rule:

A notice under Section 148 cannot be issued if three years have passed from the end of the relevant assessment year.

Cases Involving Assets, Expenditure, or Book Entries:

| S.No | Particulars | Time Limit |

|---|---|---|

| 1 | General cases | A notice under Section 148 cannot be issued if three years have elapsed from the end of the relevant assessment year. |

| 2 | Cases where the Assessing Officer possesses books of accounts, documents, or evidence showing that income chargeable to tax—represented in the form of assets, expenditure relating to a transaction or event, or entries in the books of accounts—has escaped assessment and such income amounts to ₹50 lakhs or more | A notice under Section 148 cannot be issued if ten years have elapsed from the end of the relevant assessment year. |

Examples of “income represented in the form of an asset” include land, buildings, shares, deposits, and other investments. Income represented as expenditure may relate to a particular transaction, event, or occasion. Income represented through entries may appear directly in the books of accounts.

Example:

Mr. Arjun filed his Income Tax Return for FY 2018–19 using ITR-1, disclosing only salary income. However, during the same year (AY 2019–20), he had securities sale proceeds and interest income totaling ₹20 lakhs, which were not reported. If the Assessing Officer issued a notice under Section 148 on 10 January 2023, the question arises whether such notice is valid.

Answer:

Since the income that escaped assessment is less than ₹50 lakhs, the time limit to issue notice is three years from the end of the relevant assessment year, i.e., up to 31 March 2023. As the notice was issued before this deadline, it is considered valid.

Note:

If the escaped income exceeds ₹50 lakhs, the time limit for issuing notice extends up to 31 March 2030.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Procedure to Be Followed Before Issuing Notice of Income Escaping Assessment Under Section 148A

Before issuing a notice under Section 148, the Assessing Officer (AO) must adhere to a structured sequence of steps:

Conduct an Enquiry:

The AO must conduct an enquiry regarding the income believed to have escaped assessment. In certain cases, prior approval from the specified authority may be required before beginning this enquiry.Issue a Show-Cause Notice:

The AO must serve a show-cause notice to the taxpayer under Section 148A(b), giving the taxpayer a reasonable opportunity of being heard. The notice must specify a response time, generally 7 to 30 days, although extension may be granted depending on circumstances.Consider the Taxpayer’s Reply:

The AO must examine the response, explanations, and documents provided by the taxpayer in reply to the show-cause notice.Decide Whether to Issue Notice Under Section 148:

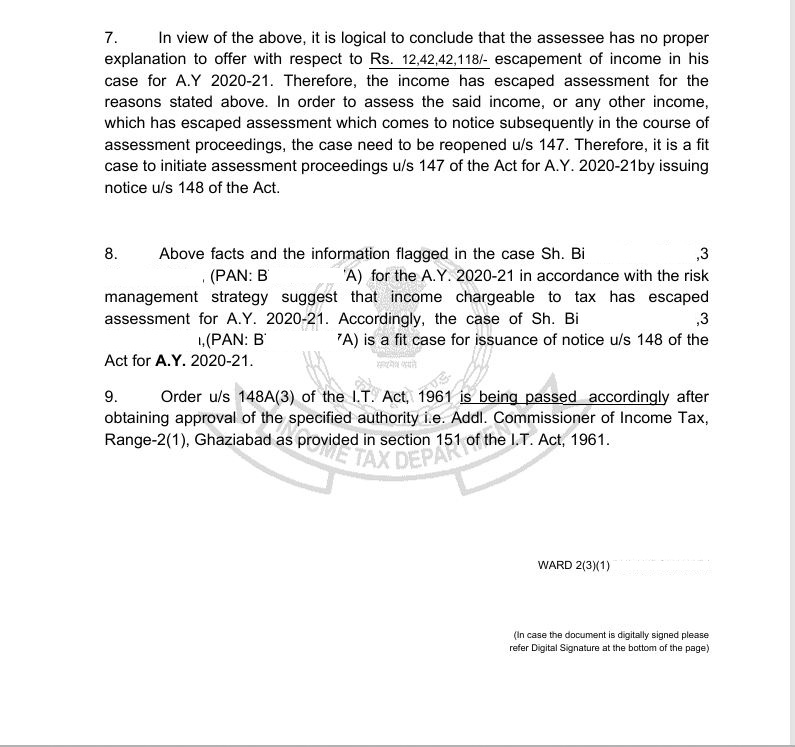

Based on the enquiry findings, available evidence, and the taxpayer’s submissions, the AO must determine whether it is appropriate to initiate reassessment. An order under Section 148A(d) must be passed with prior approval of the specified authority before issuing a formal notice under Section 148.

Time Limit for Passing an Order Under Section 148A

The Assessing Officer (AO) must adhere to strict timelines while issuing an order under Section 148A(d).

When the taxpayer furnishes a reply to the show-cause notice: The AO must pass the order within one month from the end of the month in which the taxpayer submitted the reply.

When the taxpayer does not furnish a reply: The AO must pass the order within one month from the end of the month in which the time allowed for submitting the reply expires.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Time Limit for Completion of Assessment by the Assessing Officer

For income escaping assessments, the completion deadlines depend on when the notice was served.

If the notice was served before 01/04/2019: The AO must complete the assessment within nine months from the end of the financial year in which the notice was issued.

If the notice was served on or after 01/04/2019: The AO must complete the assessment within twelve months from the end of the financial year in which the notice was issued.

Using the earlier example, the AO must complete the assessment on or before 31/03/2024.

Circumstances When Income Is Deemed to Have Escaped Assessment

The following situations are considered cases where income chargeable to tax is deemed to have escaped assessment:

When the assessee’s total income exceeds the basic exemption limit during the previous year, but no Income Tax Return has been filed.

When the assessee files a return, but the AO finds that the assessee has understated income, or has claimed excessive losses, deductions, allowances, or relief, and no assessment has previously been completed.

When the assessee has failed to furnish Form 3CEB or the report required under Section 92E for international transactions.

When information or documents received under Section 133C(2) indicate that the assessee’s income has exceeded the exemption limit, yet no return has been filed.

When a return has been filed, but the AO detects that the income has been underreported or excessive claims have been made.

When a return has been filed and assessment completed, but further information shows the assessee understated income, or claimed excessive losses, deductions, allowances, or relief.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Reasons to Believe

To invoke Section 147, the Assessing Officer must possess concrete reasons to believe, not merely reasons to suspect, that income has escaped assessment. The provision cannot be applied solely on speculative grounds or assumptions. For instance, an increase in turnover due to digital payment adoption or other reasons in the current year cannot be used to infer that income escaped assessment in earlier years. Past assessments cannot be reopened merely because a taxpayer’s turnover rose in a later year; there must be substantive evidence supporting the belief of income escapement.

Powers of AO to Assess Maximum Tax on Tax Evaders

The Assessing Officer can reassess income, make best-judgment assessments, and levy maximum permissible tax, interest, and penalties when they detect concealment of income or inaccurate particulars.

Key powers come from:

Section 143(3) – scrutiny assessment

Section 144 – best-judgment assessment for non-compliance

Section 147/148 – income escaping assessment

Section 271(1)(c) / 270A – penalty for concealment or under-reporting

The AO can tax concealed income at up to 60% + surcharge + cess under Section 115BBE, along with penalty of up to 200% of the tax in severe cases.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Prosecution Under Income Tax

AO can initiate prosecution by recommending the case to the department’s Prosecution Wing under criminal provisions of the Income Tax Act.

Key sections allowing jail for tax evasion:

Section 276C – willful attempt to evade tax (6 months to 7 years imprisonment depending on amount)

Section 277 – false statements/verification (3 months to 7 years)

Section 276CC – failure to file return (up to 7 years depending on tax evaded)

The AO’s will establish willful evasion, gather evidence, quantify evaded tax, and submit the case for prosecution; the court ultimately decides jail time.

How to Respond to an Income Tax Notice Under Section 148A

Sample Response Template for an Income Tax Notice Under Section 148A

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

DISCLAIMER

CMS Meta

Comments