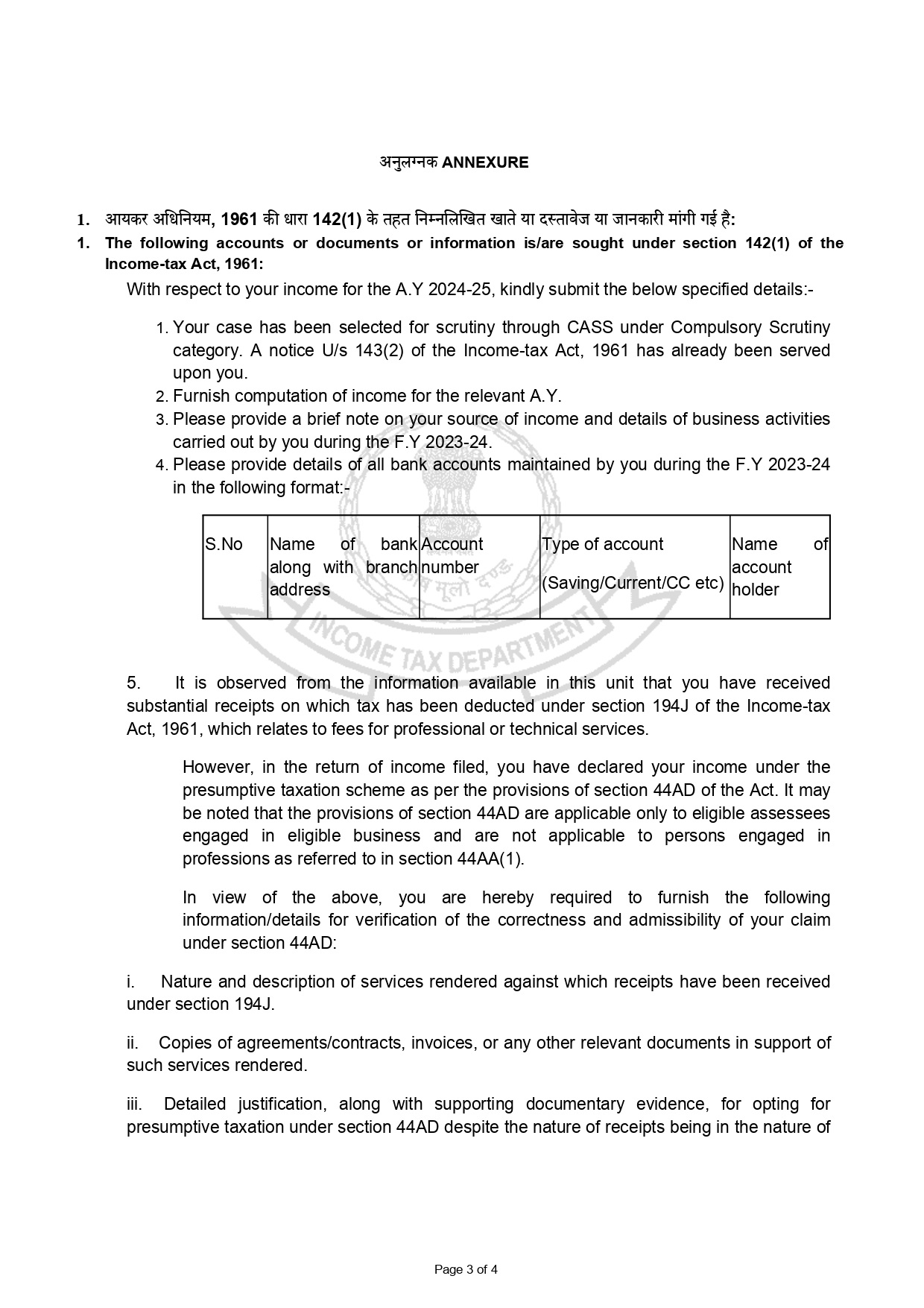

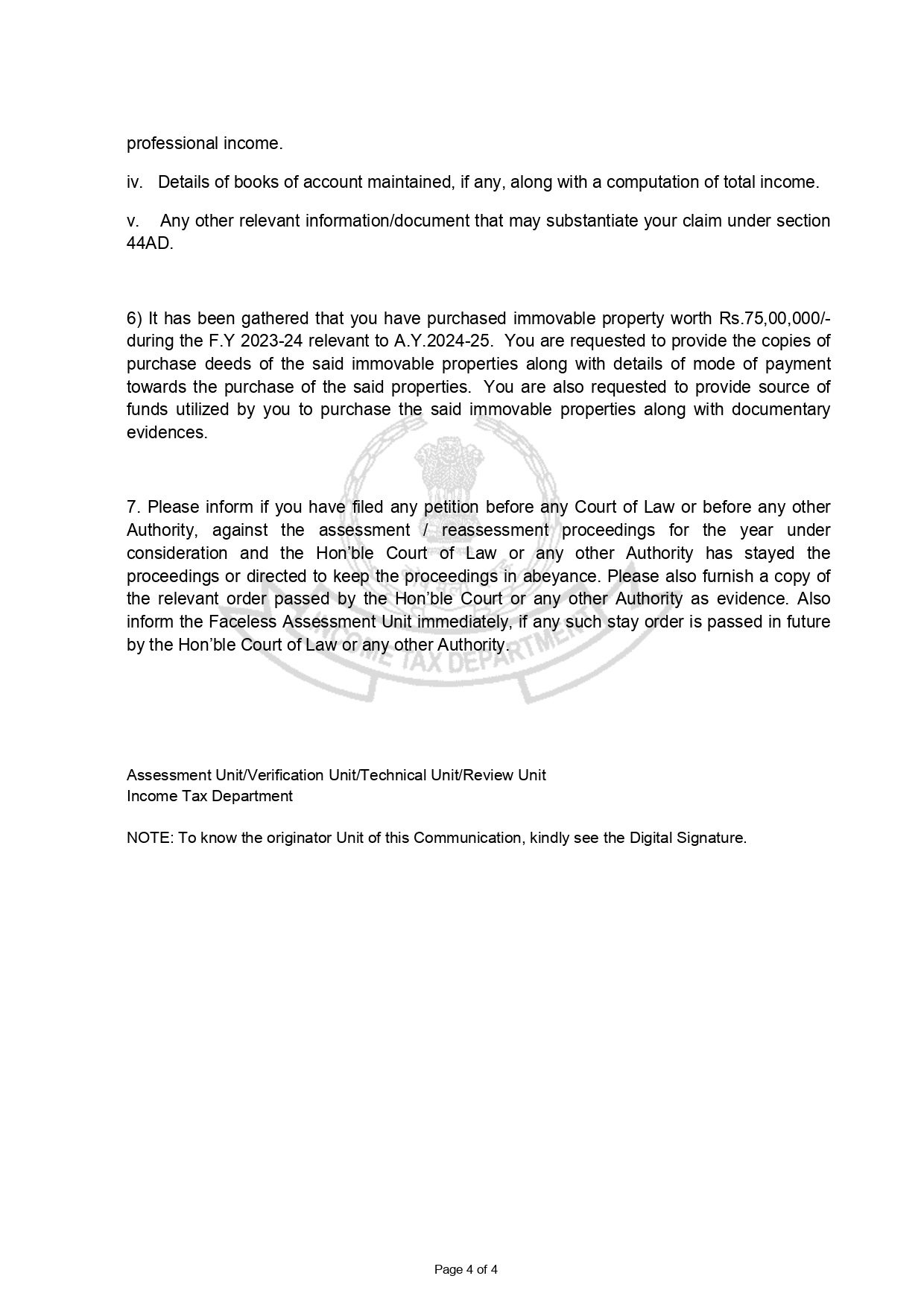

Income Tax Notice Under Section 133(6): Meaning, Causes, and How to Respond

Receiving an Income Tax Notice in India can be a stressful experience for taxpayers, as it often raises concerns about discrepancies in filed returns or potential scrutiny by tax authorities. A delay or incorrect response to such a notice can lead to severe consequences, including hefty penalties, interest charges, and even legal action in extreme cases. Ignoring the notice altogether can result in even harsher measures, such as the seizure of bank accounts, attachment of personal assets, or freezing of financial transactions by the Income Tax Department. The notice may pertain to issues like under reporting of income, fake deductions, or unexplained transactions, requiring prompt and accurate documentation. Taxpayers must carefully verify the notice type —such as intimation, scrutiny, or demand—and respond within the stipulated deadline to avoid further complications. Seeking professional assistance from a chartered accountant or tax lawyer can help in resolving the matter efficiently.

In this article, we’ll break down what an Income Tax Notice under Section 133(6) means, why it’s issued, how to respond , and provide a sample response template.

Table of Contents

- What is an Income Tax Notice?

- What is Section 133(6) of the Income Tax Act?

- Why was the Income Tax Notice Issued?

- Root Causes for Receiving a Section 133(6) Income Tax Notice

- Relevant Sections of the Income Tax Act

- How to Respond to an Income Tax Notice Under Section 133(6)

- Sample Response Template for an Income Tax Notice

- Powers of AO to Assess Maximum Tax on Tax Evaders

- Prosecution Under Income Tax

- FAQs on Income Tax Notices

- Conclusion

What is an Income Tax Notice?

An Income Tax Notice is a legal notice from the Income Tax Department requiring the taxpayer to provide additional documents, explanations, or clarifications related to their filed returns, Unexplained income or Assets or other financial transactions.

These notices are issued under various provisions of the Income Tax Act, 1961. They may relate to discrepancies in the Income Tax Return (ITR), unreported income, or random scrutiny based on your income, assets and lifestyle.

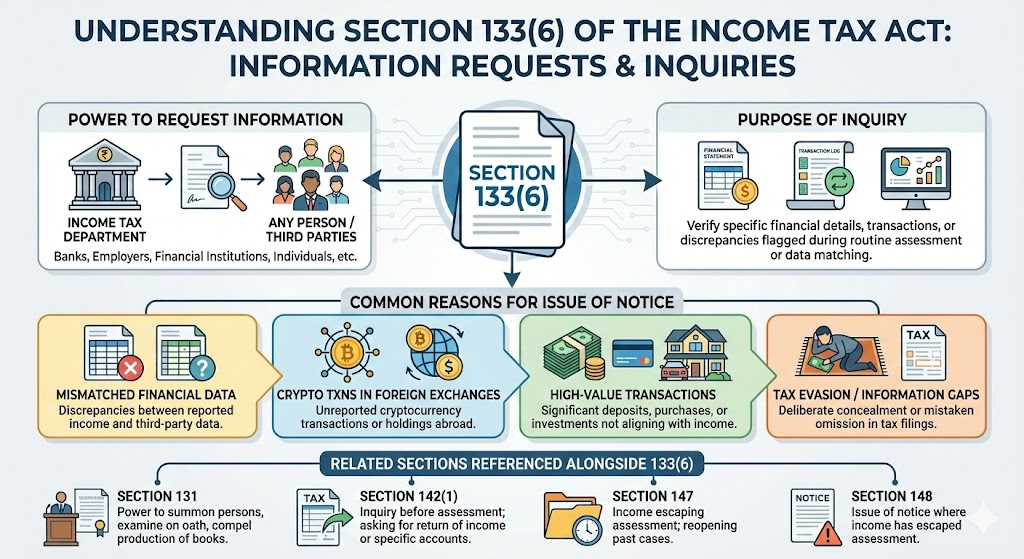

What is Section 133(6) of the Income Tax Act?

Section 133(6) of the Income Tax Act empowers the Assessing Officer (AO) to call for information from any person, including taxpayers, banks, counter parties or employers, to verify the correctness of details reported in the ITR, Bank records or any other financial records.

This is the initial stage of information gathering from your side — meaning it allows the tax authorities to gather information, even without initiating the harsher proceedings. Any information you provide will be cross-verified and could be used against you in subsequent proceedings.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

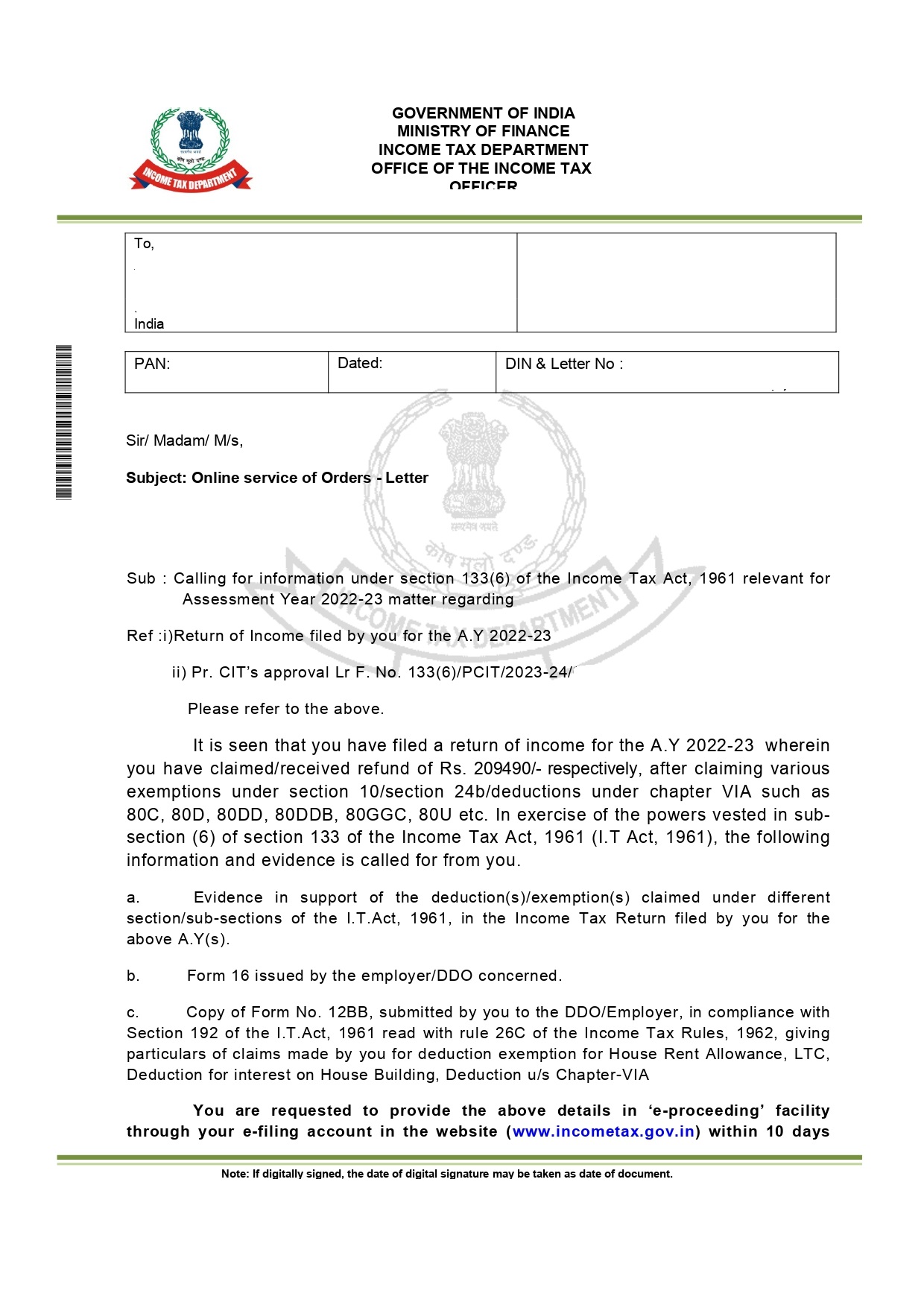

Why was the Income Tax Notice Issued?

In a recent case, Mr. ABC (name changed) received a Section 133(6) notice for the Assessment Year 2022-23.

The reasons included:

Claiming a refund of ₹2,09,490.

Claiming multiple exemptions under Section 10 (like HRA, LTC) and deductions under Section 24(b) (home loan interest) and Chapter VI-A (80C, 80D, 80DD, 80DDB, 80GGC, 80U).

The department requested Mr. ABC to provide:

Proof of deductions/exemptions claimed.

Form 16 from his employer.

Form 12BB (details of claims for exemptions/deductions submitted to the employer).

This helps the Assessing Officer confirm whether the refund claimed is justified.

Root Causes for Receiving a Section 133(6) Income Tax Notice

1. Mismatch in Claimed Deductions

If deductions claimed in the ITR do not match what is reported by your employer in Form 16 or Form 12BB, the department may issue a notice.

2. Large Refund Claims

Higher-than-usual refund claims often trigger scrutiny.

3. Incorrect or Incomplete ITR

Missing or incorrect entries related to HRA, home loan interest, or donations can lead to verification notices.

4. Random Scrutiny

Cases are also selected randomly for verification, especially those with multiple deduction claims.

5. Third-Party Mismatch

If banks, employers, or other third parties report information different from what you’ve declared, a notice may be issued. This is a common reason why several Crypto P2P traders are receiving notices and facing harsh penalties.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Relevant Sections of the Income Tax Act

1. Section 133(6) – Power to Call for Information

Purpose:

Section 133(6) of the Income Tax Act gives the Assessing Officer (AO) the authority to request information from any person — including taxpayers, banks, companies, or even third parties — if such information may help in any inquiry or assessment.

Key Features:

This section can be invoked even if no assessment proceedings are pending against the taxpayer.

It is primarily used to verify discrepancies or gather additional details.

The information sought could include bank account statements, salary details, rent receipts, loan documents, etc.

Example:

Suppose Mr. ABC claims House Rent Allowance (HRA) of ₹1.8 lakh, but no rent agreement is submitted. The AO may issue a notice under Section 133(6) asking for rent receipts, rental agreement, and landlord details.

Why It Matters:

This section ensures that taxpayers substantiate their claims and prevents fraudulent claims of deductions or exemptions.

2. Section 10 – Income Not Included in Total Income (Exemptions)

Purpose:

Section 10 provides tax exemptions for certain types of income, ensuring they are not added to the total taxable income.

Common Exemptions Under Section 10:

Section 10(13A): House Rent Allowance (HRA) – Exemption is based on rent paid, salary, and city of residence.

Section 10(10): Gratuity – Exempt up to prescribed limits.

Section 10(10AA): Leave Encashment – Exemption up to a certain threshold.

Section 10(10D): Life Insurance Maturity Proceeds – Exempt if conditions are met.

Section 10(5): Leave Travel Concession (LTC) – For travel within India by employees.

Example:

If an employee earns a basic salary of ₹40,000/month and pays ₹20,000/month as rent in a metro city, a part of their HRA may be exempt under Section 10(13A).

Why It Matters:

Incorrect or exaggerated claims under Section 10 often trigger scrutiny notices. Supporting documents (rent receipts, travel tickets, etc.) are essential to validate these claims.

3. Section 24(b) – Deduction on Home Loan Interest

Purpose:

Section 24(b) allows taxpayers to claim deductions on interest paid on home loans for self-occupied or rented properties.

Key Provisions:

Self-occupied Property: Deduction up to ₹2 lakh per year.

Let-out Property: No upper limit on interest deduction (entire interest amount is deductible).

Loan must be taken for purchase, construction, or renovation of property.

Conditions:

The loan should be from a recognized financial institution or lender.

Construction of the house should be completed within 5 years from the end of the financial year in which the loan was taken.

Example:

If Mr. ABC has a housing loan of ₹25 lakh with an annual interest of ₹2.4 lakh, he can claim ₹2 lakh as deduction under Section 24(b) for a self-occupied property.

Why It Matters:

To claim this deduction, taxpayers must submit a home loan interest certificate from their lender. Missing or invalid certificates may lead to scrutiny.

4. Sections 80C–80U (Chapter VI-A) – Deductions for Investments, Expenses, and Donations

Purpose:

These sections offer deductions from gross total income, reducing overall tax liability. They cover a wide range of investments, medical expenses, donations, and specific personal expenditures.

Popular Deductions:

Section 80C: Up to ₹1.5 lakh for investments in PF, PPF, ELSS, life insurance premiums, tuition fees, home loan principal repayment, etc.

Section 80D: Health insurance premium deduction:

₹25,000 for self and family (₹50,000 for senior citizens).

Section 80DD & 80DDB: Medical treatment for disabled dependents or specified diseases.

Section 80G: Donations to charitable institutions (50%-100% deduction, depending on the organization).

Section 80U: Deduction for individuals with disabilities (up to ₹1.25 lakh).

Example:

If Mr. ABC invests ₹1 lakh in ELSS, pays ₹25,000 as health insurance premium, and donates ₹20,000 to a registered NGO, he can claim combined deductions under Sections 80C, 80D, and 80G.

Why It Matters:

Supporting documents like investment proofs, medical bills, and donation receipts must be preserved to justify these claims if queried by the department.

5. Section 272A(2)(c) – Penalty for Non-Compliance

Purpose:

This section imposes a penalty for failure to comply with notices issued by the Income Tax Department.

Key Provision:

Penalty of ₹500 per day for non-compliance with a notice under Section 133(6) (or other similar sections).

The penalty continues until the taxpayer submits the requested information.

Example:

If Mr. ABC fails to respond to a notice for 15 days, the penalty could amount to ₹7,500 (₹500 × 15 days).

Why It Matters:

Ignoring notices can lead not only to monetary penalties but also to further scrutiny or reassessment of your ITR.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

How to Respond to an Income Tax Notice Under Section 133(6)

Step 1: Read the Notice Carefully

Identify the section under which it’s issued, specific documents requested, and the submission deadline.

Step 2: Collect Documents

Step 3: Verify Your ITR

Step 4: Submit Online via e-Proceedings

Step 5: Consult an Experienced CA or Tax Lawyer

If the notice involves complex discrepancies, schedule an appointment with our CAs to discuss your notice and case details. CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India.

Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Sample Response Template for an Income Tax Notice

Subject: Response to Notice under Section 133(6) for AY 2022–23

To:

The Income Tax Officer

[Ward/City]

Respected Sir/Madam,

Powers of AO to Assess Maximum Tax on Tax Evaders

The Assessing Officer can reassess income, make best-judgment assessments, and levy maximum permissible tax, interest, and penalties when they detect concealment of income or inaccurate particulars.

Key powers come from:

Section 143(3) – scrutiny assessment

Section 144 – best-judgment assessment for non-compliance

Section 147/148 – income escaping assessment

Section 271(1)(c) / 270A – penalty for concealment or under-reporting

The AO can tax concealed income at up to 60% + surcharge + cess under Section 115BBE, along with penalty of up to 200% of the tax in severe cases.

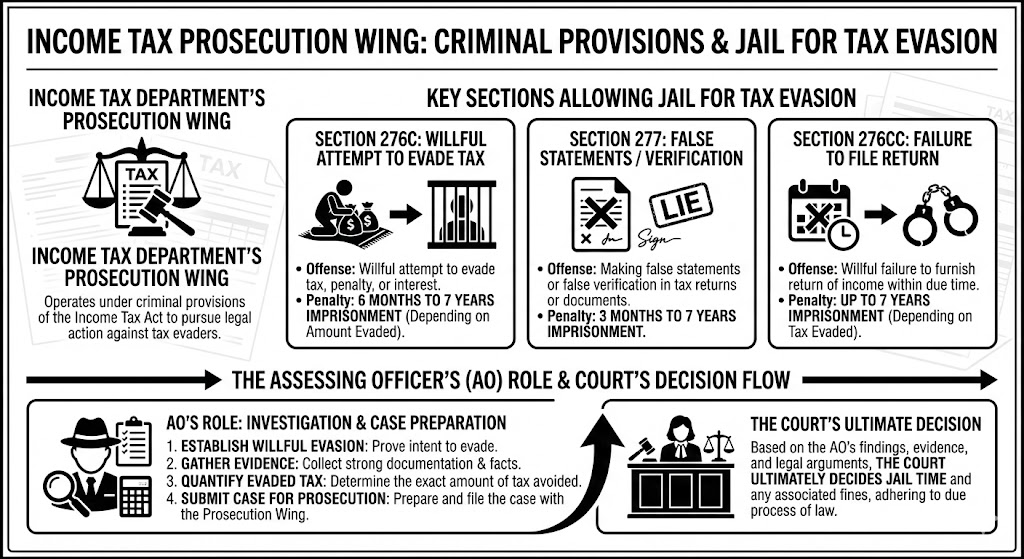

Prosecution Under Income Tax

AO can initiate prosecution by recommending the case to the department’s Prosecution Wing under criminal provisions of the Income Tax Act.

Key sections allowing jail for tax evasion:

Section 276C – willful attempt to evade tax (6 months to 7 years imprisonment depending on amount)

Section 277 – false statements/verification (3 months to 7 years)

Section 276CC – failure to file return (up to 7 years depending on tax evaded)

The AO’s will establish willful evasion, gather evidence, quantify evaded tax, and submit the case for prosecution; the court ultimately decides jail time.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

FAQs on Income Tax Notices

1. What is Section 133(6) of the Income Tax Act?

It empowers the Assessing Officer to request information from any taxpayer or third party on issues like underreporting of income, fake deductions, or unexplained transactions, requiring prompt and accurate response.

2. How do I respond to an Income Tax Notice?

Log in to the income tax portal, go to e-proceedings, and upload the requested documents within the timeline mentioned in the notice.

3. What happens if I don’t respond to a notice?

Non-compliance can result in a penalty of ₹500 per day under Section 272A(2)(c) and may lead to further scrutiny.

4. Does receiving a notice mean I am in trouble?

It would depend on the nature of the details sought by the Assessing Officer. Underreporting of income, false deductions, and unexplained transactions have become common methods of tax evasion among individuals. This issue is further exacerbated in the case of P2P transactions, where individuals fail to comply with TDS requirements, and most sellers (of USDT) do not file income tax returns.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Conclusion

As mentioned above, Underreporting of income, false deductions, and unexplained transactions have become common methods of tax evasion among individuals. This issue is further exacerbated in the case of Crypto Trading done on Foreign Exchanges and on DeFi Networks, Crypto P2P transactions, where individuals fail to comply with TDS requirements, and most sellers (of USDT) do not file income tax returns. An Income Tax Notice under Section 133(6) is primarily a investigation tool followed by assessment order by the department to confirm the correctness of your claims. A proper response ensures smooth closure of the matter.

Pro Tip: Always maintain proper records of your investments, loans, and exemptions claimed in your ITR to avoid future notices.

DISCLAIMER

CMS Meta:

Comments