Types of Income Tax Notices - 2026 India

In this article we will discuss various Types of Income Tax Notices and their meaning. We will also cover some FAQ on Income Tax Notices

Table of Contents

- Types of Income Tax Notices

- Notice u/s 139(9) - Defective Income Tax Return

- Notice u/s 142(1) - Inquiry before Assessment

- Notice u/s 143(1) - Intimation

- Notice u/s 143(2) - Scrutiny

- Notice u/s 148 - Income Escaped Assessment

- Notice u/s 156 - Demand Notice

- Notice u/s 245 - Refund Adjusted against the Tax Demand

- Difference between Income Tax Notice and Assessment

- Section 143(3) - Scrutiny Assessment

- Section 144 - Best Judgement Assessment

- Section 131(1A) - Income is concealed or likely to be concealed

- Frequently Asked Question (FAQ) on Income Tax Notices

- What exactly is an income-tax notice?

- How Should You Handle Income Tax Notices from the IT Department?

- What is the purpose of an income-tax notice?

- How do I find out if an income-tax notice has been issued to me or what the status of the notice is?

- Can I get more than an Assessment Year Income Tax Notice?

- If I don't know an income tax notice, what could happen?

- What are my chances of receiving a notification from the Income Tax Department?

- How long is the notice of income tax received from me normally taken?

- I am currently living outside of India; how should I approach the Income-tax Department in this situation?

- What is a limited Scrutiny?

- When is the Notice Sent to The Assessee?

- How to deal with the Notice u/s 142(1)?

- Notices being received by our Crypto clients u/s 142 (1) and u/s 148A

- What are the penalties for non-compliance with Section 142(1) Tax Notice?

- What is the time limit for income tax notice?

- Why Only Expert Tax Consultants Should Handle Your IT Scrutiny Notice?

- Conclusion

Types of Income Tax Notices

Notice u/s 139(9) - Defective Income Tax Return

In this case, the Assessing Officer (AO) is of the opinion that ITR filed by the assessee is defective then he may issue notice u/s 139(9). AO also shares the proper error description along with the probable solution to rectify the same. The defect u/s 139(9) can be because of the wrong ITR filed, wrong or non declaration of Income as per Form 26AS, missing information, incomplete return etc.

The Assessee is given an opportunity to respond within 15 days from the date of intimation and if he don't respond within stipulated time, the AO will consider the return invalid and proceed for assessment.

Assessee may agree or disagree with the observation of the AO. If you can agree, you can file a return after rectifying the defect in the return.

Notice u/s 142(1) - Inquiry before Assessment

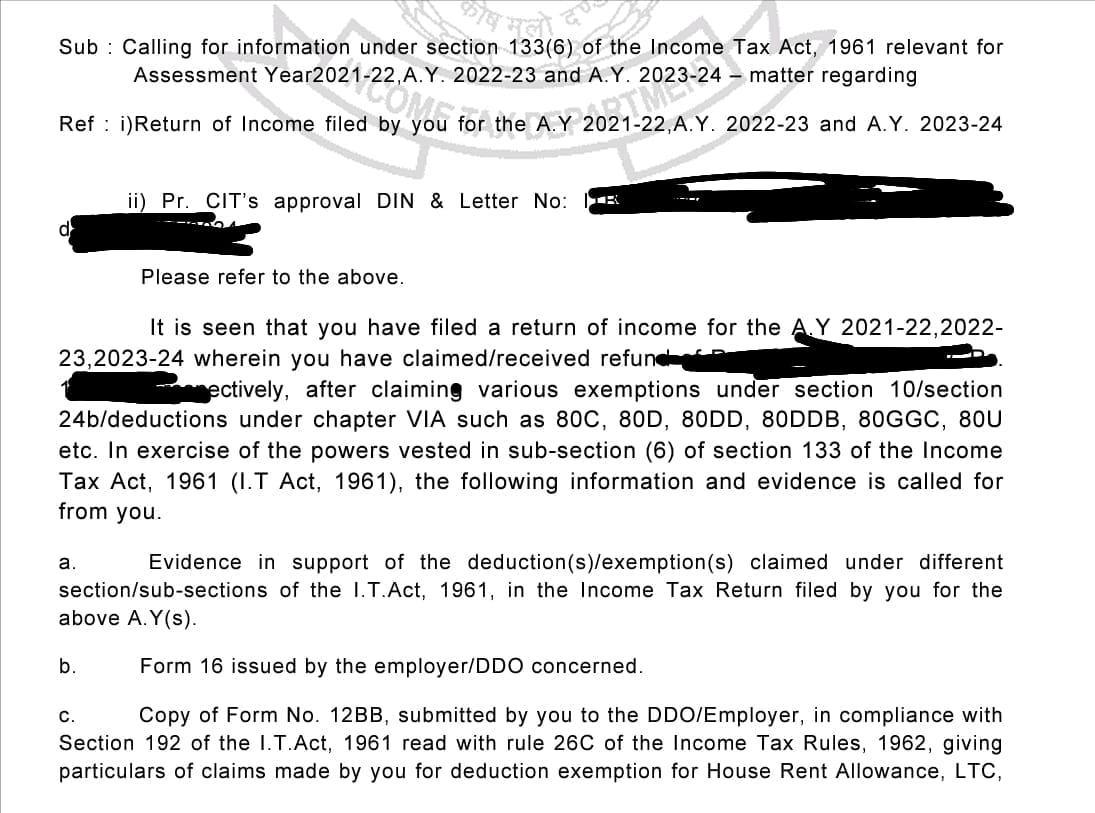

The purpose of this notice is to request additional information and documentation from the taxpayer in order to complete the processing of their filed return. This notice will also be sent to compel a taxpayer to furnish additional documents and details. Also, if the Assessee has not filed their return on time, they will receive a notice for a preliminary inquiry u/s 142(1). The time limit to serve the notice u/s 142(1) is before the end of the relevant assessment year.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions and penalties.

Notice u/s 143(1) - Intimation

Notice u/s 143(1) is one of the most common income tax notice that is frequently received by taxpayers from the income tax department, it requires a response to rectify errors, incorrect claims, or inconsistencies in a filed income tax return. If an individual receives this notice and wishes to amend their return, they have a 15-day window to do so. Otherwise, the tax return will be processed after incorporating the necessary adjustments specified in the notice.

Notice u/s 143(2) - Scrutiny

If the Assessee's response to the Income Tax Notice u/s 142(1) is deemed unsatisfactory by the Assessing Officer or if the Assessee fails to provide the requested documents, they will receive a notice u/s 143(2).

There can be 3 types of following notices under Section 143(2):

Limited Scrutiny: This is a Computer-Assisted Scrutiny Selection (CASS) where cases are selected based on set parameters. The scrutiny will be limited to the particular area of return mentioned in the notice. An example of this scrutiny can be a mismatch in tax credits, inaccurate information, etc.

Complete Scrutiny: A complete scrutiny is carried out on the return filed along with all supporting documents. Cases are flagged based on CASS. The scope of scrutiny is not limited to these types of notices. However, the assessing officer cannot verify documents beyond the particular assessment year.

Manual Scrutiny: Cases are selected for complete scrutiny based on the criteria defined by the Central Board of Direct Taxes; the criteria may vary every year.

Taxpayers who receive notice under Section 143(2) will have to submit additional information. The Assessee or their authorized representative may file a reply through the portal as physical submissions are no longer required, and the process will be conducted exclusively through E-Assessment.

Notice u/s 148 - Income Escaped Assessment

In situations where the assessing officer suspects that the income disclosed by an individual is incorrect, resulting in underpayment of taxes, or if the individual has failed to file a return despite being legally obligated to do so, then he will issue notice u/s 148 and it is considered as income escaping assessment. In such cases, the assessing officer has the authority to assess or reassess the income. Before proceeding with the assessment or reassessment, the officer must serve a notice to the assessee requesting them to provide their income return. This notice is issued under Section 148 of the income tax provisions.

The notice can be served within 4 years / 6 years / 16 years from the end of the relevant assessment year.

Notice u/s 156 - Demand Notice

If any penalty, tax, fine or any other amount is due from the taxpayer to the Income Tax Department then Income Tax notice u/s 156 is served. Normally this notice is served after the assessment of ITR. The taxpayer can deposit the amount payable within 30 days from the date of the Income Tax notice. There is no time limit to serve this notice. Income tax notice u/s 143(1) and 200A are also referred as Notice of Demand.

Notice u/s 245 - Refund Adjusted against the Tax Demand

It is basically an Intimation from the Income Tax Department. This notice is issued when the tax refund (full/partial) for an assessment year is adjusted against the tax demand due from the taxpayer. It is issued in cases where the assessing officer suspects that tax payment has been evaded in previous years and wishes to offset the current year's refund against the outstanding demand, a notice u/s 245 may be issued.

However, such an adjustment can only be made after the individual has been given a proper notice and a chance to be heard. The recipient of the notice is required to respond within 30 days of receiving it. Failure to do so may be considered as implied consent by the assessing officer and the assessment process may be initiated accordingly. As such, it is recommended to respond to the notice promptly.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

Difference between Income Tax Notice and Assessment

| Notice | Assessment |

| An income tax notice is a written communication sent by the Income Tax Department to a taxpayer alerting an issue with his tax account. The notice can be sent for different reasons like filing/ non-filing their income tax return, making the assessment, asking for certain details, etc. | Once the return of income is filed up by the taxpayer, the next step is the processing of the return of income by the Income Tax Department. The process of examining the return of income by the Income-Tax department is called as “Assessment”. |

Section 143(3) - Scrutiny Assessment

Under section 143(3) of the Income Tax Act, Assessment refers to a detailed examination, commonly known as scrutiny assessment. In this Assessment, a thorough investigation of the return of income is conducted to verify the accuracy and authenticity of various claims, deductions, and other details provided by the taxpayer in their return of income.

The scope of assessment under section 143(3) primarily aims to confirm that the taxpayer has not understated their income, computed excessive losses, or underpaid taxes in any manner. To establish this, the Assessing Officer carries out a meticulous review of the return of income, carefully assessing the various claims, deductions, and other details provided by the taxpayer to ensure their accuracy and genuineness.

Detailed procedure of assessment under section 143(3)?

The notice under section 143(2) must be served within six months from the end of the financial year in which the return is filed. The taxpayer or their representative will then appear before the Assessing Officer to present their arguments and supporting evidence on various matters and issues as required by the Assessing Officer.

After hearing and verifying the evidence and taking into account all relevant materials gathered by the Assessing Officer, an assessment of the taxpayer's total income or loss will be made, and the sum payable by the taxpayer or the refund due to them will be determined based on the assessment. This assessment is made by the Assessing Officer in writing.

Section 144 - Best Judgement Assessment

Notice u/s 144 of the Income Tax Act 1961 is commonly referred to as Best Judgement Assessment or Ex Parte Assessment. In simple terms, if a taxpayer fails to respond to Income Tax notices or provide the documents and details requested, the Income Tax officer can proceed with an assessment and issue a demand notice based on their understanding, without seeking any further information from the taxpayer. This scenario can be particularly disadvantageous for the taxpayer, as they will be at a disadvantage if they wish to appeal the decision. Appealing can be both a costly and time-consuming activity for the taxpayer.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

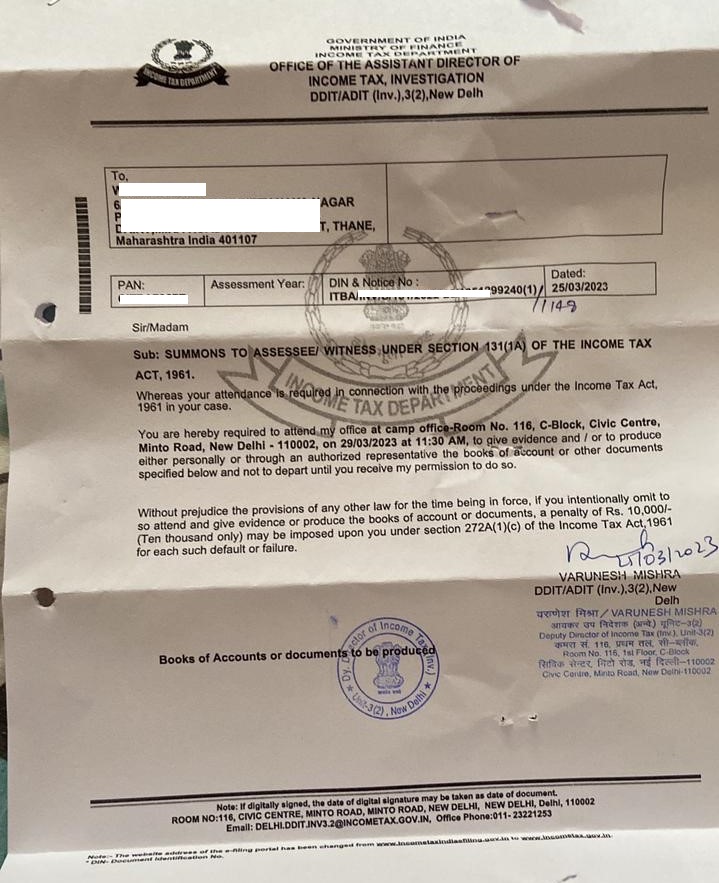

Section 131(1A) - Income is concealed or likely to be concealed

If the AO is of the opinion that the assessee is concealing the Income or likely to conceal Income then you will receive Income Tax notice u/s 131(1A). This notice is basically an intimation that AO is initiating an enquiry or investigate into the matter.

The assessing office can impound the books of account or other documents by providing reasons for the same. There is no specific time limit to serve this notice.

Before we move to FAQs on Income Tax Notices, lets summarise in this table the various Types of Income Tax Notices we have discussed today:

| Type of Notice | Description |

| Notice u/s 143(1) - Intimation | This is one of the most commonly received income tax notices. The income tax department sends this notice seeking a response to the errors/ incorrect claims/ inconsistencies in an income tax return that was filed.If an individual wants to revise the return after receiving this notice, it must be done within 15 days.Else, the tax return will be processed after making the necessary adjustments mentioned in the 143(1) tax notice. |

| Notice u/s 142(1) - Inquiry | This notice is addressed to the assessee when the return is already filed and further details and documents are required from the assessee to complete the process.This notice can also be sent to necessitate a taxpayer to provide additional documents and information. |

| Notice u/s 139(1) - Defective Return | An income tax notice under Section 139(1) would be issued if the income tax return filed does not contain all necessary information or incorrect information. |

| If tax notice under Section 139(1) is issued, you should rectify the defect in the return within 15 days. | |

| Notice u/s 143(2) - Scrutiny | An income tax notice under Section 143(2) is issued if the tax officer was not satisfied with the documents and information that was submitted by the taxpayer.Taxpayers who receive notice under Section 142(2) have been selected for detailed scrutiny by the Income Tax department and will have to submit additional information. |

| Notice u/s 156 - Demand Notice | This type of income tax notice is issued by the Income Tax Department when any tax, interest, fine, or any other sum is owed by the taxpayer.All demand tax notice will stipulate the sum which is outstanding and due from the taxpayer. |

| Notice Under Section 245 | If the officer has reason to believe that tax has not been paid for the previous years and he wants to set off the current year's refund against that demand, a notice u/s 245 can be issued.However, the adjustment of demand and refund could be done only if the individual has been provided proper notice and an opportunity to be heard. The recipient has to respond to the notice is 30 days from the day of receipt of the notice.If the individual does not respond within the specified timeline, the assessing officer can consider this as consent and proceed with the assessment.Therefore, it is advisable to respond to the notice at the earliest. |

| Notice Under Section 148 | The officer may have a reason to believe that you have not disclosed your income correctly and therefore, you have paid lower taxes.Or the individual may not have filed his return at all, even if you must have filed it as per law. This is termed as income escaping assessment. Under these circumstances, the assessing officer is entitled to assess or reassess the income, according to the case.Before making such an assessment or reassessment, the assessing officer should serve a notice to the assessee asking him to furnish his return of income.The notice issued for this purpose is issued under the provisions of Section 148. |

Frequently Asked Question (FAQ) on Income Tax Notices

What exactly is an income-tax notice?

The Income-tax Department processes an individual's / assessee's (also known as a taxpayer's) income-tax return when it is filed. If a mistake, inaccuracy, or inconsistency is discovered in the income-tax return filed, the Assessee is notified by way of an income-tax notice. The Income-tax Department issues a variety of income-tax notices, which you can read about in the question below.

How Should You Handle Income Tax Notices from the IT Department?

A brief overview of IT Notices and the reasons for issuing them. The most essential thing to keep in mind when receiving an IT notification is that almost everything is now linked to Aadhaar, PAN, Bank Accounts, Digital Wallets, and Mobile Numbers. The Income Tax Department is evolving into a highly developed, well-connected tax system on a daily basis. Typical Reasons for Receiving an IT Notice- A quick reminder to file your tax returns

- Randomly scrutinize

- Inconsistency in your tax returns

- Errors in TDS Amount Deducted

- Errors in TDS Amount Deducted

- Requesting documentation proof

- Transactions of high value that do not match income.

- Transfer of property on behalf of the wife or children

- High Gift Transaction Number

- Non-payment of the entire tax amount before the due date

- Return of income tax not filed or filed after the date of the due date

- Asset not divulged.

- Foreign income not disclosed

- Family Member Investments

What is the purpose of an income-tax notice?

An income-tax notification may be issued for the following reasons2. Errors or discrepancies in the income tax return you filed.

How do I find out if an income-tax notice has been issued to me or what the status of the notice is?

Here's how to find out if you've gotten an income-tax notice or intimation in a few easy steps:- Sign-up / Login at https://portal.incometaxindefiling.gov.in

- From the top menu, go to "My Account" and select from the download the option "View e-filed returns/forms."

- For the relevant evaluation year click "Ack. No."

- Your return is subject to correction if you have any of the following messages. B. the ITR filed is defective/incomplete. A. In the meantime, U/S 143(1)(a) B. C. Completed and determined request ITR processing.

Can I get more than an Assessment Year Income Tax Notice?

Yes, for the same valuation year, you can receive more than one revenue tax notice. For instance, the intimation 143(1) on your income tax has been requested and you filed a correction for it. If you do, however, refuse to do so, you will receive a second Revenue Tax Advisory/Order 154, which requires further clarification from the income tax department.If I don't know an income tax notice, what could happen?

We recommend that you should not neglect any income-tax notices. Ignoring any notices of income tax may result in the 1961 Income Tax Act penalty and prosecution.What are my chances of receiving a notification from the Income Tax Department?

The Income Tax Department sends notices to less than 1% of all taxpayers. You are notified of income tax if:- You must file your return on income tax and have not submitted the same return.

- There is an error in your return

- Wrong TDS credit is taken the return you have filed.

- The Assessing Officer shall request any documents or details.

- Any other situation considered fit by the evaluating officer

How long is the notice of income tax received from me normally taken?

No specific deadline for the resolution of any income tax notice issued is established by the income tax department. It would be fully dependent on different circumstances such as the Income Tax Department processing time, the assesses response time, and so on.

I am currently living outside of India; how should I approach the Income-tax Department in this situation?

Filing a rectification of an income-tax return and responding to an income-tax notification are now both done online and can be done from anywhere in the world. If you are unable to appear in person at an Income-tax office, you can appoint someone to act as your representative in India and ask that person to appear before the assessing officer with all of your required documentation.What is a limited Scrutiny?

In cases where the Income Tax office requires examination of only specific entries or a limited scope of income, as opposed to all the related details, it is termed as "Limited Scrutiny" in an Income Tax return. A limited scrutiny order is issued to initiate such an examination. For instance, if there is a sale of a house that is not reflecting in the Income Tax return filed by the taxpayer, a limited scrutiny order may be issued to investigate the matter.

When is the Notice Sent to The Assessee?

Section 142(1) tax notice is usually served in the following scenarios:

Scenario 1 - Where the return has not been filed at all

Where the asessee has not filed the return, but the income tax officer feels that he qualifies to file their income tax return and purposely or by mistake forgotten to file the IT return than the officer can issue this notice u/s 142(1) to file a proper IT return

So if you have received a notice under this section, you have to first file the proper income tax return and then you need to submit supporting documents and provide information as asked by the assessing the offer as the assessment proceeds.

Scenario 2 - Where the return has been filed within the due time

If You receive income tax notice U/s 142 (1) even when you have filed the income tax return, that means the IT officer found something a miss in your IT return. There is something missing as per the income tax officer (Assessing Officer) or he is not having all the information, all the documents on the basis of which you have filed the income tax return. The Assessing Officer is unable to check whether your return is proper or some income has been missed out or some income has been evaded.

In this situation, he will ask the assessee to provide supporting documents and information on basis of which he has filed the return and will like to cross-check if he has filed a proper IT return with well-supported documents.

How to deal with the Notice u/s 142(1)?

If you got this Notice, should you worry about that? Yes, because generally income tax department does not issue notice without proper cause, they got something serious where they feel at least more than One Lakh Rupees or more of income is under-reported. And they can add that much income in your income and claim taxes to be paid. That means they got some substantial information and that’s why they are issuing a Notice to know more from you.

After the assessee has received the notice from the income tax department, he must furnish the required documents under inquiry. The taxpayer is given a reasonable opportunity of responding with supporting documents that may be needed based on such an inquiry.

In case you have already filed the return and still you received the income tax notice u/s 142 (1), then in that case again you have to do your computation again. This would mean that you resubmit all your bank statements and all supporting docs and prepare a detailed response to the department on their queries. You should prepare a new computation and compare it with your old return and see whether something has missed out or not. It may be dividend income or maybe some interest income or maybe some shares you sold. It can also be related to the property was sold, but you forget to mention. These all could be the basis of why you receive the income tax demand notice under Section 142.

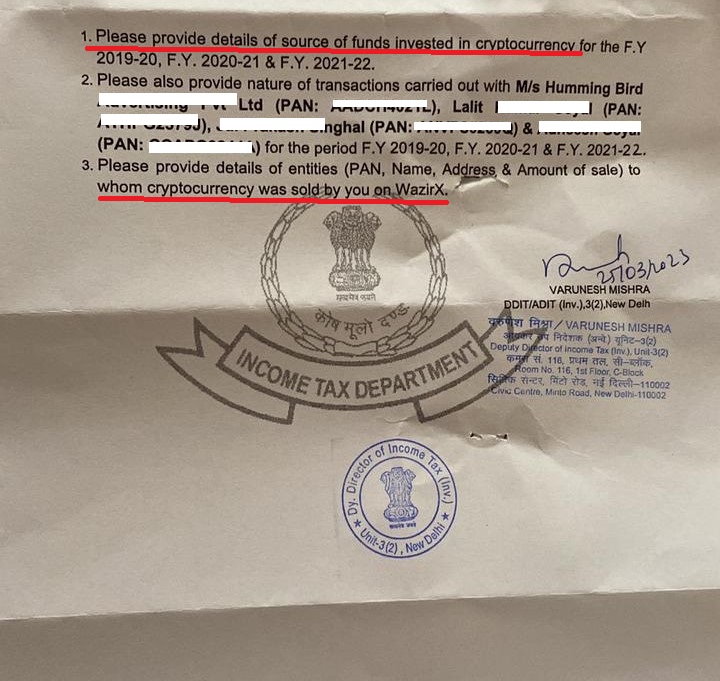

The Income Tax Department of India has been sending notices to cryptocurrency investors who have not reported their crypto investments and gains in their tax returns. Failure to report crypto investments and gains can lead to penalties and legal consequences.

It is important for crypto investors in India to understand their tax obligations and to report their crypto investments and gains accurately in their tax returns. If you have received a notice from the Income Tax Department, it is advisable to schedule a call with our tax professional to understand your options and to ensure that you comply with tax laws.

Notices being received by our Crypto clients u/s 142 (1) and u/s 148A

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

What are the penalties for non-compliance with Section 142(1) Tax Notice?

Section 142(1) covers the penalties for non-filing of required documents within the time frame, Such a tax notice may result in Best Judgment Assessment u/s 144.

Further, if a taxpayer fails to comply with the notice issued under Section 142(1), the Income Tax Department may initiate penalty proceedings under Section 271(1)(b) of the Income Tax Act. The penalty for non-compliance with Section 142(1) is Rs. 10,000. However, the penalty amount may vary depending on the taxpayer's income and other circumstances of the case.

In addition to the penalty, the Income Tax Department may also initiate prosecution proceedings under Section 276CC of the Income Tax Act. If found guilty, the taxpayer may face imprisonment for a term ranging from three months to two years and may also be liable to pay a fine.

Therefore, it is essential for taxpayers to comply with the notice issued under Section 142(1) and file their tax returns within the specified time to avoid penalties and prosecution proceedings.

What is the time limit for income tax notice?

1 - Upto four years from the end of the relevant Assessment Year

2 - After four years but upto six years from the end of the relevant Assessment Year

Notice can only be issued by the Chief Commissioner or Commissioner if they are satisfied that income has escaped assessment, and the amount of income which has escaped assessment should be more than Rs. 1,00,000, beyond four years but up to six years from the end of the relevant AY. For AY 2017-18, notice under section 148 can be issued till 31st March 2024.

3 - After four years but up to sixteen years from the end of the relevant AY

Notice under section 148 can be issued beyond four years but up to sixteen years from the end of the relevant AY if income in relation to any asset (including financial interest in any entity) located outside India, is chargeable to tax in India but has escaped assessment. For AY 2017-18, notice under section 148 can be issued till 31st March 2034.

Why Only Expert Tax Consultants Should Handle Your IT Scrutiny Notice?

Before entrusting a consultant with the responsibility of responding to your tax notice, it is imperative to evaluate their prior experience in handling similar cases and their corresponding outcomes. It is important to note that a consultant with only expertise in tax return filing may not possess the necessary skills to effectively manage scrutiny notices. At CA Mitesh & Associates, we have a dedicated team, led by an experienced Chartered Accountant, that specializes in managing income tax notices and scrutiny related cases. Therefore, you can be confident that your case will not be an experiment for us.

Conclusion

As you can see that there are various types of Income Tax Notices and assessments that are issued under various sections of Income Tax and they all have various repercussions and penalties. All Income Tax Notices are to be taken very seriously and should be responded in timely fashion to avoid adverse action against you.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that we are not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. CA Mitesh and Associates is India's leading Cryptocurrency Taxation Firm which is committed to helping people navigate complex tax laws and banking regulations. Our main aim is to assist the individuals with applicable laws & regulations compliance and providing support at each & every level to make sure that they stay compliant and grow continuously. For any query, help or feedback you may get in touch here - Appointment with CA. Please note the all consultations with the CA are Paid consultations. Financial Year 2025.

Comments