Appeals under the Income Tax Act: Sections, Structure, and the Critical Importance of Filing Them Correctly

The appellate framework under the Income Tax Act, 1961 is a carefully designed, multi-tier system that allows taxpayers to challenge orders passed by tax authorities. Given the complexity of tax assessments and the wide range of disputes—from additions under Section 69A to penalties under Section 271AAC—this framework acts as a crucial safeguard for ensuring fairness, accountability, and legal correctness.

However, while the right to appeal is fundamental, it is equally important that appeals are filed under the correct section, before the correct authority, within the prescribed time, and in the proper format. Errors in any of these aspects can lead to dismissal, delays, or even permanent loss of legal remedies.

This article provides a comprehensive overview of the different sections governing appeals and explains why precision in filing is not merely procedural—but absolutely critical.

Table of Contents

- 🔹 1. First Appeal: Section 246A

- 🔹 2. Appeal under Section 246

- 🔹 3. Appeal under section 253

- 🔹 4. Appeal under section 260A

- 🔹 5. Appeal under section 261

- 🔹 6. Very Important Sections 264 and 263 in the Appeals Process

- 🔹 Why It Is Extremely Important to File Appeals Correctly

- 1. Jurisdictional Accuracy

- 2. Limitation Period (Time Sensitivity)

- 3. Proper Form and Documentation

- 4. Correct Grounds of Appeal

- 5. Impact on Penalty Proceedings

- 6. Preservation of Legal Rights

- 7. Financial Implications

- 8. Strategic Litigation Planning

- 9. Digital Compliance and DIN Linking

- 10. Judicial Discipline and Precedent

- 🔹 Conclusion

🔹 1. First Appeal: Section 246A

(Commissioner of Income Tax – Appeals)

Scope and Applicability

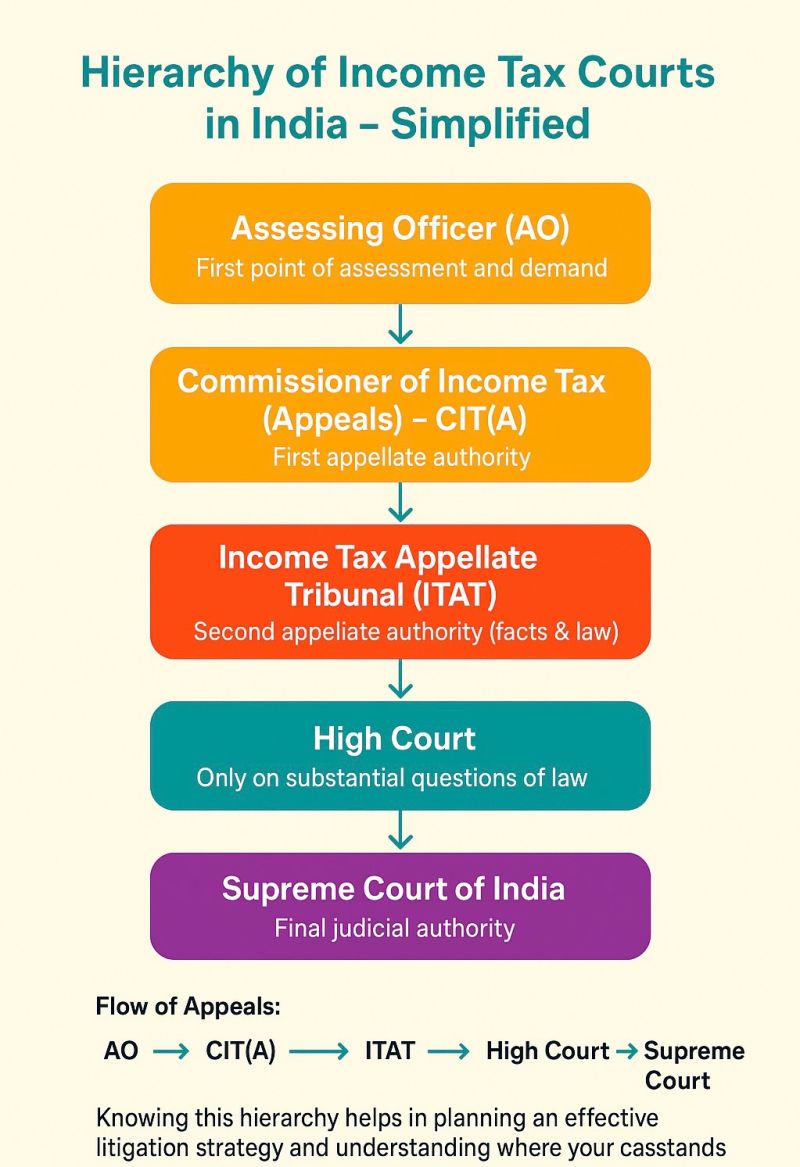

Section 246A is the cornerstone of the appellate mechanism. It provides the assessee with the right to appeal against a wide range of orders passed by the Assessing Officer (AO).

Orders Appealable under Section 246A

These include:

Assessment orders under Sections 143(3), 144

Reassessment orders under Section 147

Intimations under Section 143(1), where adjustments are made

Penalty orders (e.g., Sections 270A, 271AAC, etc.)

Orders under Section 154 (rectification)

TDS/TCS related orders

The appeal is filed before the Commissioner of Income Tax (Appeals), commonly referred to as CIT(A).

Procedure

Filed using Form 35

Time limit: 30 days from date of order/service of notice

Requires payment of prescribed appeal fee

Importance

Section 246A is often the first and most critical opportunity to contest an adverse order. It is also the stage where factual records, evidences, and legal arguments are most thoroughly examined.

🔹 2. Appeal under Section 246

Appeal before Joint Commissioner (Appeals). Section 246 provides for appeals before the Joint Commissioner (Appeals), a relatively recent addition aimed at reducing litigation burden and speeding up resolution for smaller cases.

Key Features

- Applicable in cases where jurisdiction is specifically assigned

- Designed for low to mid-value disputes

- Powers are broadly similar to CIT(A)

Practical Note

Although not as widely used as Section 246A, this provision is increasingly relevant as the government explores decentralization of appellate functions.

🔹 3. Appeal under section 253

Income Tax Appellate Tribunal. Once the first appeal is decided, either party—assessee or department—can approach the Income Tax Appellate Tribunal under Section 253.

Scope

Appeals can be filed against:

- Orders of CIT(A)

- Orders passed by Principal Commissioner or Commissioner under certain sections (e.g., Section 263)

Nature of ITAT

- Final fact-finding authority

- Independent quasi-judicial body

- Can examine both facts and law

Procedure

- Filed in prescribed form (Form 36)

- Time limit: 60 days from receipt of CIT(A) order

Importance

This is often the stage where complex legal and factual disputes are conclusively analyzed. Proper presentation of evidence and arguments becomes crucial.

🔹 4. Appeal under section 260A

An appeal can be filed before the High Court of India under Section 260A.

Key Condition

- Appeal must involve a “substantial question of law”

This means:

- Interpretation of statutory provisions

- Legal validity of actions

- Procedural irregularities affecting legality

Purely factual disputes are not entertained.

Time Limit

- 120 days from receipt of ITAT order

Importance

This stage shifts focus from facts to legal interpretation. A well-drafted appeal must clearly articulate the substantial question of law involved.

🔹 5. Appeal under section 261

The final appellate authority is the Supreme Court of India and the appeal needs to be filed under section 261.

When Applicable

- When High Court certifies the case as fit for appeal

- Or via Special Leave Petition (SLP) under constitutional provisions

Importance

Decisions at this level set binding precedents for the entire country.

🔹 6. Very Important Sections 264 and 263 in the Appeals Process

While not strictly “appeals,” revisions provide alternative remedies. These sections provide revision mechanism.

Section 264 (Revision by Assessee)

- Filed before Commissioner

- Can be used when no appeal has been filed

- Provides discretionary relief

Section 263 (Revision by Commissioner)

- Initiated by department

- For orders that are “erroneous and prejudicial to the interests of revenue”

🔹 Why It Is Extremely Important to File Appeals Correctly

Filing an appeal is not just about disagreeing with an order—it is about invoking a statutory right in a legally valid manner. Even minor procedural errors can have serious consequences.

1. Jurisdictional Accuracy

Each section corresponds to a specific authority. Filing under the wrong section or before the wrong authority can result in:

- Rejection of appeal

- Transfer delays

- Loss of limitation period

For example, a penalty order appeal must be filed under Section 246A before CIT(A). Filing elsewhere is invalid.

2. Limitation Period (Time Sensitivity)

Appeals are strictly time-bound:

- 30 days (CIT(A))

- 60 days (ITAT)

- 120 days (High Court)

Delay requires a condonation application, which may or may not be accepted.

Failure to file within time can lead to:

- Dismissal of appeal

- Finality of incorrect tax demand

3. Proper Form and Documentation

Each appellate stage requires specific forms:

- Form 35 (CIT(A))

- Form 36 (ITAT)

Incorrect or incomplete filing can lead to:

- Defective appeal notices

- Dismissal for non-compliance

4. Correct Grounds of Appeal

The “grounds of appeal” define the scope of the dispute.

Poorly drafted grounds can:

- Limit arguments

- Prevent raising key issues later

- Weaken the case significantly

Each ground must be:

- Specific

- Legally sustainable

- Linked to facts

5. Impact on Penalty Proceedings

Incorrect or delayed appeals can directly affect penalty cases.

For instance:

- If quantum addition is not challenged properly

- Penalty under Section 271AAC or 270A may become unavoidable

Conversely:

- A valid appeal can justify keeping penalty proceedings in abeyance

6. Preservation of Legal Rights

Appeals are hierarchical. Missing one stage can block access to higher remedies.

Example:

- If CIT(A) appeal is not filed

- Direct appeal to ITAT is generally not permitted

Thus, each step must be correctly followed.

7. Financial Implications

Incorrect filing can lead to:

- Immediate tax recovery

- Interest accumulation

- Penalties

Whereas proper filing can:

- Stay demand

- Provide relief

- Reduce financial burden

8. Strategic Litigation Planning

Appeals are not just reactive—they are strategic.

A well-planned appeal:

- Anticipates future litigation stages

- Builds a consistent narrative

- Preserves evidence and arguments

9. Digital Compliance and DIN Linking

Modern tax administration relies on:

- Document Identification Numbers (DIN)

- E-filing portals

Errors in quoting DIN, PAN, or assessment year can invalidate filings or delay processing.

10. Judicial Discipline and Precedent

Higher appellate authorities rely on:

- Properly framed questions

- Consistent legal arguments

Incorrect filing can:

- Dilute legal issues

- Lead to adverse precedents

🔹 Conclusion

The appellate system under the Income Tax Act, 1961 is both a right and a responsibility. Sections such as 246A, 253, 260A, and 261 create a structured pathway for dispute resolution, ensuring that taxpayers have multiple opportunities to seek justice.

However, this system operates within strict procedural boundaries. Filing an appeal is not a mere formality—it is a technical exercise requiring precision, legal understanding, and strategic thinking.

In today’s environment of increased scrutiny, automated systems, and stringent timelines, even small errors can have disproportionate consequences. Therefore, whether it is choosing the correct section, drafting proper grounds, or adhering to timelines, every aspect of the appeal process must be handled with care.

A correctly filed appeal does not just challenge an order—it preserves rights, controls financial exposure, and lays the foundation for successful litigation.

DISCLAIMER

The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that we are not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. CA Mitesh and Associates is India's leading Crypto Taxation Firm which is committed to helping people navigate complex tax laws and banking regulations. Our main aim is to assist the individuals with applicable laws & regulations compliance and providing support at each & every level to make sure that they stay compliant and grow continuously. For any query, help or feedback you may get in touch here - Appointment with CA. Please note the all consultations with the CA are Paid consultations. 2026

Comments