Case Study - F&O Trader Overcomes Tax Assessment Challenges

About the Case

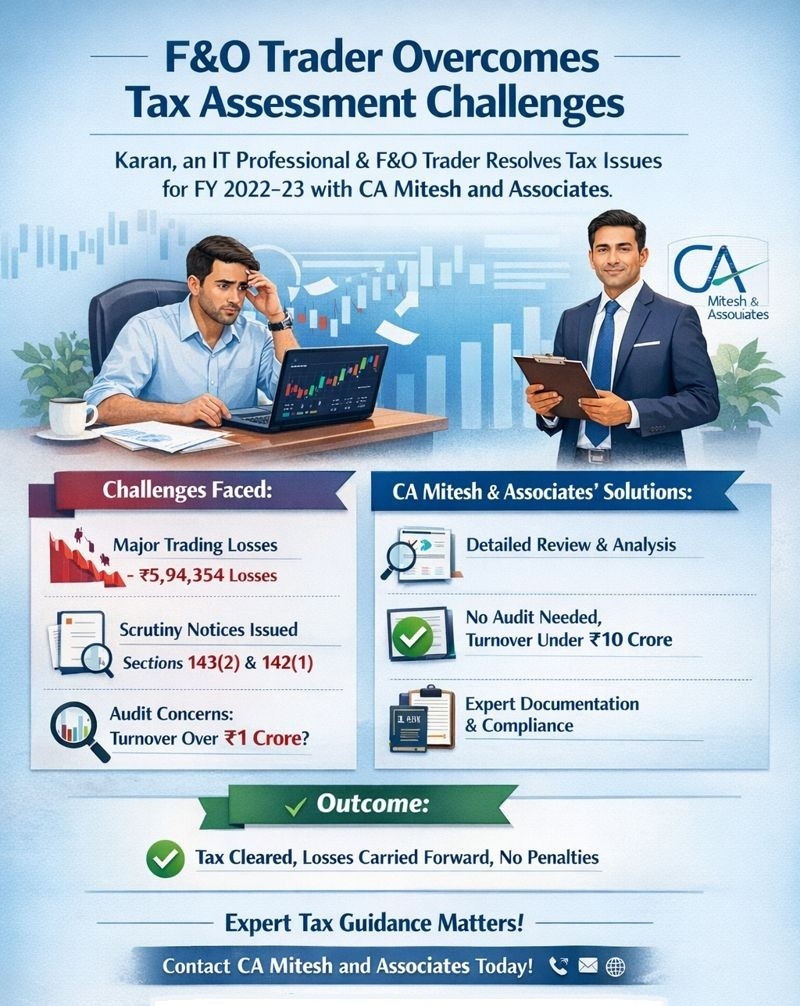

This case study highlights the journey of Karan, an IT professional and Futures & Options (F&O) trader, who successfully navigated a complex income-tax assessment for FY 2022–23 with the expert support of CA Mitesh and Associates.

Table of Contents

Background

In the ever-evolving and intricate landscape of taxation, individuals often struggle to interpret and comply with regulatory requirements. Karan, an IT professional with an active interest in F&O trading, encountered significant tax challenges during the financial year 2022–23. After receiving scrutiny notices and facing uncertainty, he sought professional guidance from CA Mitesh and Associates, marking the beginning of a structured and successful resolution of his tax issues.

Challenges Faced

These are few challenges faced by Karan – an F&O Trader

Alongside his career as an IT professional, Karan actively participated in the complex world of F&O trading.

Due to the volatile nature of the market, he incurred substantial trading losses. While the declared loss stood at INR 3,77,694, the actual loss amounted to INR 5,94,354.

His difficulties escalated when he received scrutiny notices under Sections 143(2) and 142(1) of the Income-tax Act, bringing his return under the Computer-Assisted Scrutiny Selection (CASS).

The tax authorities sought detailed explanations and supporting documents to validate the declared losses and income.

A major point of contention was the applicability of a tax audit under Section 44AB, as his F&O turnover exceeded INR 1 crore. The department questioned why an audit had not been conducted.

The situation demanded in-depth technical knowledge of tax laws, precise documentation, and expert representation—making professional assistance essential.

How CA Mitesh and Associates Helped

We adopted a comprehensive and methodical approach:

In-depth Review: A detailed examination of Karan’s income-tax returns, financial statements, bank records, and broker-issued profit & loss statements was undertaken to understand the complete financial picture.

Expert Advisory: It was established that a tax audit under Section 44AB was not required, as Karan’s turnover was below INR 10 crore and over 95% of his F&O transactions were conducted digitally—making the INR 1 crore audit threshold inapplicable.

Documentation & Compliance: All required submissions were meticulously prepared and filed. Relevant judicial precedents and case laws were cited to support the explanations provided, ensuring transparency and full regulatory compliance throughout the assessment proceedings.

Outcome

Successful Assessment: The Income-tax Department accepted Karan’s declared income and losses without any modifications.

Complete Relief: There were no additions to total income, no penalties or demands raised, and the carried-forward losses were allowed to continue—bringing the matter to a smooth and favorable conclusion.

Conclusion

Karan’s case underscores the critical importance of professional expertise when dealing with complex tax scrutiny and compliance issues. The timely intervention and deep technical knowledge of CA Mitesh and Associates ensured a seamless assessment process, allowing Karan to focus on his profession and trading activities without unnecessary stress. This case study clearly demonstrates the value of expert tax consultancy in resolving challenging income-tax assessments.

Call to Action

Facing income-tax scrutiny or complex tax notices?

Connect with CA Mitesh and Associates for reliable, expert-driven tax consulting services—and resolve your tax challenges with confidence and ease.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return Filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

DISCLAIMER

The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that we are not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. CA Mitesh and Associates is India's leading Crypto Taxation Firm which is committed to helping people navigate complex tax laws and banking regulations. Our main aim is to assist the individuals with applicable laws & regulations compliance and providing support at each & every level to make sure that they stay compliant and grow continuously. For any query, help or feedback you may get in touch here - Appointment with CA. Please note the all consultations with the CA are Paid consultations. 2026

CMS Meta

Comments