How to reply to Income Tax Notice u/s 142 (1)

Notices are issued by the income tax department under the various provisions of the Income Tax Act to the assesses with the purpose to assure greater tax compliances. You may benefit by reading this article on Types of Income Tax Notices a person may receive from Income Tax Department.

This article covers notices being sent by Income Tax Department under section 142 of the income tax act, some sample notices being received by crypto investors, how to deal with such notices and penalties for non-compliance.

Table of Contents

When is the Notice Sent to The Assessee?

Section 142(1) tax notice is usually served in the following scenarios:

Scenario 1 - Where the return has not been filed at all

Where the asessee has not filed the return, but the income tax officer feels that he qualifies to file their income tax return and purposely or by mistake forgotten to file the IT return than the officer can issue this notice u/s 142(1) to file a proper IT return

So if you have received a notice under this section, you have to first file the proper income tax return and then you need to submit supporting documents and provide information as asked by the assessing the offer as the assessment proceeds.

Scenario 2 - Where the return has been filed within the due time

If You receive income tax notice U/s 142 (1) even when you have filed the income tax return, that means the IT officer found something a miss in your IT return. There is something missing as per the income tax officer (Assessing Officer) or he is not having all the information, all the documents on the basis of which you have filed the income tax return. The Assessing Officer is unable to check whether your return is proper or some income has been missed out or some income has been evaded.

In this situation, he will ask the assessee to provide supporting documents and information on basis of which he has filed the return and will like to cross-check if he has filed a proper IT return with well-supported documents.

How to deal with the Notice u/s 142(1)?

If you got this Notice, should you worry about that? Yes, because generally income tax department does not issue notice without proper cause, they got something serious where they feel at least more than One Lakh Rupees or more of income is under-reported. And they can add that much income in your income and claim taxes to be paid. That means they got some substantial information and that’s why they are issuing a Notice to know more from you.

After the assessee has received the notice from the income tax department, he must furnish the required documents under inquiry. The taxpayer is given a reasonable opportunity of responding with supporting documents that may be needed based on such an inquiry.

In case you have already filed the return and still you received the income tax notice u/s 142 (1), then in that case again you have to do your computation again. This would mean that you resubmit all your bank statements and all supporting docs and prepare a detailed response to the department on their queries. You should prepare a new computation and compare it with your old return and see whether something has missed out or not. It may be dividend income or maybe some interest income or maybe some shares you sold. It can also be related to the property was sold, but you forget to mention. These all could be the basis of why you receive the income tax demand notice under Section 142.

The Income Tax Department of India has been sending notices to cryptocurrency investors who have not reported their crypto investments and gains in their tax returns. Failure to report crypto investments and gains can lead to penalties and legal consequences.

It is important for crypto investors in India to understand their tax obligations and to report their crypto investments and gains accurately in their tax returns. If you have received a notice from the Income Tax Department, it is advisable to schedule a call with our tax professional to understand your options and to ensure that you comply with tax laws.

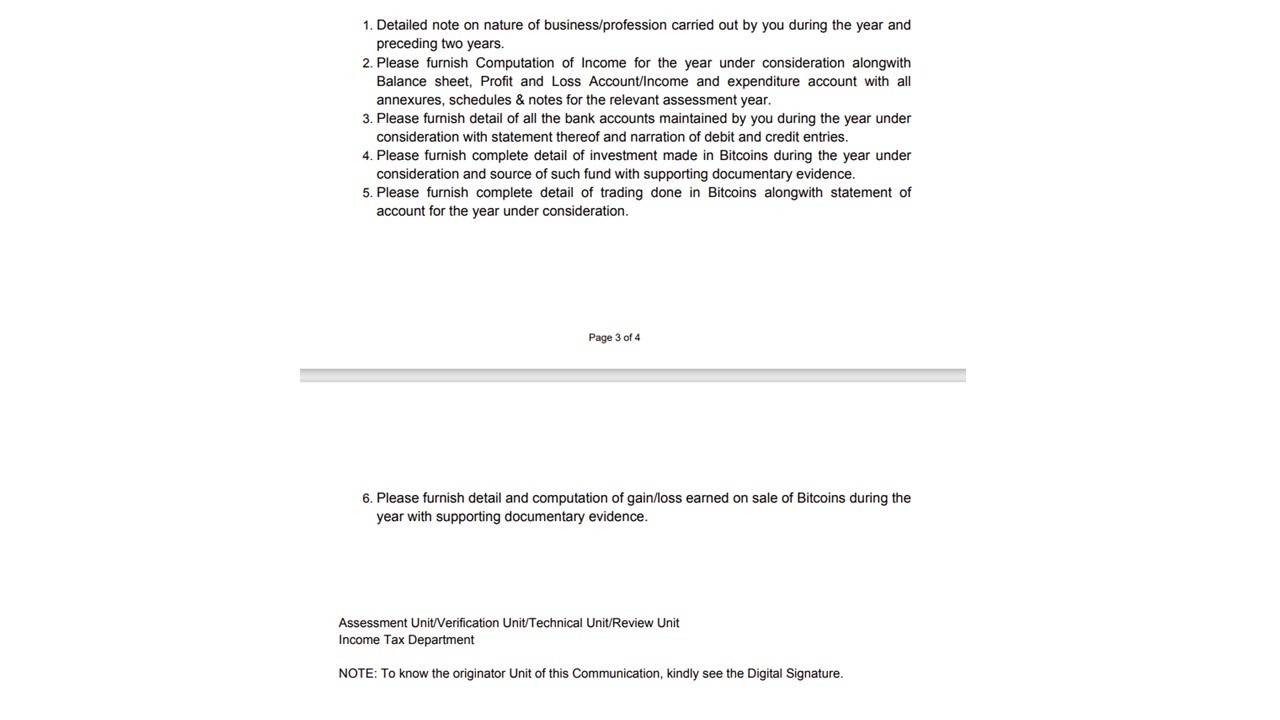

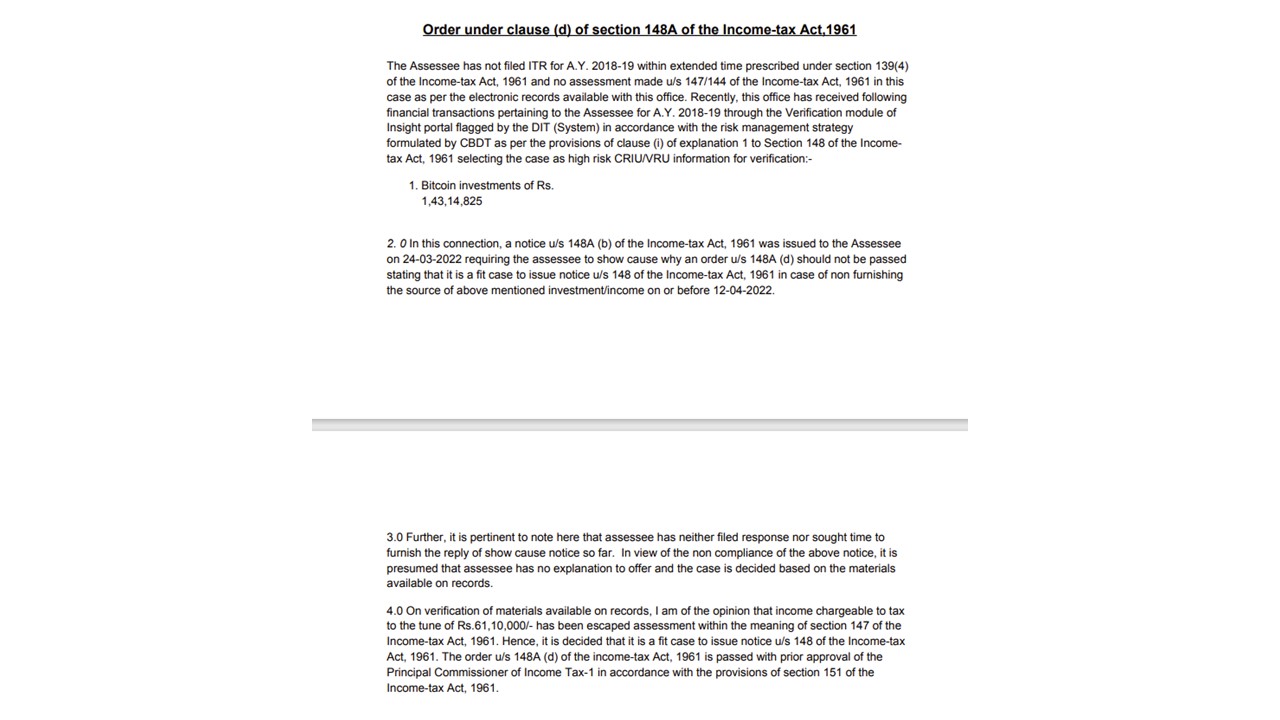

Notices being received by our Crypto clients u/s 142 (1) and u/s 148A

What are the penalties for non-compliance with Section 142(1) Tax Notice?

Section 142(1) covers the penalties for non-filing of required documents within the time frame, Such a tax notice may result in Best Judgment Assessment u/s 144.

Further, if a taxpayer fails to comply with the notice issued under Section 142(1), the Income Tax Department may initiate penalty proceedings under Section 271(1)(b) of the Income Tax Act. The penalty for non-compliance with Section 142(1) is Rs. 10,000. However, the penalty amount may vary depending on the taxpayer's income and other circumstances of the case.

In addition to the penalty, the Income Tax Department may also initiate prosecution proceedings under Section 276CC of the Income Tax Act. If found guilty, the taxpayer may face imprisonment for a term ranging from three months to two years and may also be liable to pay a fine.

Therefore, it is essential for taxpayers to comply with the notice issued under Section 142(1) and file their tax returns within the specified time to avoid penalties and prosecution proceedings.

DISCLAIMER

The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that we are not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. CA Mitesh and Associates is Mumbai's leading Cryptocurrency Taxation Firm which is committed to helping people navigate complex tax laws and banking regulations. Our main aim is to assist the individuals with applicable laws & regulations compliance and providing support at each & every level to make sure that they stay compliant and grow continuously. For any query, help or feedback you may get in touch here - Appointment with CA. Please note the all consultations with the CA are Paid consultations. Financial Year 2023.

Comments