ITR Forms Acknowledge Crypto Income with Dedicated Section

The recently released 2023 ITR Forms have separate section for crypto income. This interesting change is seen in Income Tax Return Form 1 (ITR-1) and Income Tax Return Form 2 (ITR-2) so far. A separate schedule has been added for reporting income from crypto and other Virtual Digital Assets (VDA).

Table of Contents

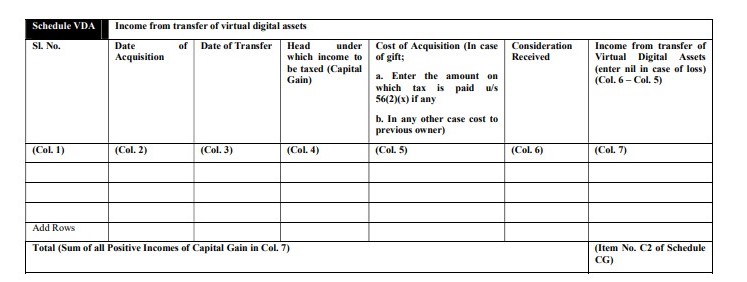

Schedule VDA - Income from transfer of Virtual Digital Assets / Crypto

The separate schedule for VDA requires details like date of acquisition, date of transfer, Head under which income to be taxed (Capital Gain), Cost of acquisition (in case of gift), Consideration received, and Income from transfer of Virtual Digital Assets and in case of loss you can enter the NIL value. It is to be filled in by a person who is in receipt of amounts or in other words by individuals who have sold any any crypto in previous year.

Be aware that Virtual Digital Assets shall comprise all the cryptos such as Bitcoin, Ethereum, etc, and other digital assets such as Non-fungible token (NFTs).

This is how the Schedule VDA - Income from transfer of Virtual Digital Assets / Crypto looks like:

In India, income from cryptocurrency is considered taxable under the Income Tax Act, 1961. The tax treatment of cryptocurrency income in India depends on the nature of the income, i.e., whether it is considered as capital gains or business income.

If an individual buys and sells cryptocurrency as an investment, any gains or losses arising from the sale of cryptocurrency would be considered as capital gains.

On the other hand, if an individual is engaged in the business of buying and selling cryptocurrency, the income earned from such activities is considered as business income, and will be taxed accordingly.

It is important to note that cryptocurrency income must be disclosed while filing income tax returns in India. Failure to disclose such income can attract penalties and prosecution under the Income Tax Act.

Taxation of Cryptocurrency or Virtual Digital Assets in India from Financial Year 2022-23

The entire 30% tax on any crypto assets will be deducted from the profits earned via various crypto tokens in an entire financial year. Also NO deduction will be allowed any expenditure or allowance for cryptocurrency (other than the cost of acquisition). Further, the government has clarified that if one incurs any loss from the transfer of virtual assets, it cannot be set off against any other income.

So far this new section is seen on CBDT’s New ITR 1 and ITR 2 forms for AY 2023-24.

Income Tax Return Form 1 (ITR-1)

ITR-1 form is also known as ITR-1 Sahaj form and is specified for people who have an income of up to ₹50 lakhs from the following sources :

- Income from salary/pension

- Income from one house property (excluding cases where loss is brought forward from previous years)

- Income from other sources (excluding winning from lottery and income from race horses)

- In the case of clubbed Income Tax Returns, where a spouse or a minor is included, this can be done only if their income is limited to the above specifications.

Income Tax Return Form 2 (ITR-2)

- Income from salary or pension

- Income from house property

- Income from capital gains

- Income from other sources (including lottery winnings)

- Foreign income or assets

In addition to the above, ITR-2 is also applicable for those individuals or HUFs who do not have income from business or profession.

Therefore, if you are an individual or HUF and have income from any of the above sources, you are eligible to file ITR-2 for the Assessment Year 2023-24.

Conclusion

Crypto Investors, Traders and Taxpayers in general can start working to estimate tax liability and disclosure required in ITR forms. The timely release of income tax return forms also indicates that Income Tax Department expects taxpayers to do their filing soon after the financial year ends and NOT to expect extension beyond 31 July 2023.

The contents of this article are for information purposes only and do not constitute an advice or a legal opinion and are personal views of the author. It is based upon relevant law and/or facts available at that point of time and prepared with due accuracy & reliability. Readers are requested to check and refer relevant provisions of statute, latest judicial pronouncements, circulars, clarifications etc before acting on the basis of the above write up. The possibility of other views on the subject matter cannot be ruled out. By the use of the said information, you agree that we are not responsible or liable in any manner for the authenticity, accuracy, completeness, errors or any kind of omissions in this piece of information for any action taken thereof. CA Mitesh and Associates is Mumbai's leading Cryptocurrency Taxation Firm which is committed to helping people navigate complex tax laws and banking regulations. Our main aim is to assist the individuals with applicable laws & regulations compliance and providing support at each & every level to make sure that they stay compliant and grow continuously. For any query, help or feedback you may get in touch here - Appointment with CA. Please note the all consultations with the CA are Paid consultations. Financial Year 2024.

Comments