Non-Disclosure of Foreign Assets in ITR – Black Money Act & Tax Implications for NRIs

Non-Disclosure of Foreign Assets in ITR – Black Money Act & Tax Implications – NRIs, Returning NRIs, Resident Indians

- The Mandatory Obligation: Disclosing Global Wealth

- Requirement Disclosure of Foreign Assets In ITR

- What is The Black Money Act?

- The Severe Consequences of Non-Compliance: Enter the Black Money Act

- Foreign Assets Investigation Unit (FAIU) – Proceedings To Investigate Foreign Assets Transactions

- Landmark Case - Shobha Harish Thawani v. JCIT

- Detailed Real Life scenario of an NRI Client Regarding Foreign Asset Disclosure Notices

A significant number of individuals who fall under the diverse categories of Non-Resident Indians (NRIs)—particularly those specifically known as "Returning NRIs" who are permanently relocating back to their homeland—as well as various Foreign Citizens, including those holding status as Overseas Citizens of India (OCIs), Persons of Indian Origin (PIOs), and other expatriates, often find themselves in a changing legal landscape. When these individuals either decide to permanently return back to the geographical boundaries of India to settle down, or simply come to reside within India for an extended, prolonged duration of time for professional or personal reasons, their official status undergoes a fundamental shift in the eyes of the tax authorities. According to the complex and detailed stipulations laid out in the Income Tax provisions of India, specifically regarding residential status, these individuals transition from being classified as non-residents to officially becoming recognized as Tax Residents in India for that specific financial year.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

The Mandatory Obligation: Disclosing Global Wealth

As soon as this critical transition in status occurs, and these former NRIs or Foreign Citizens meet the necessary criteria to be categorized as Tax Residents in India, a new and substantial set of legal obligations immediately applies to them that did not exist previously. The most critical and often overlooked of these new obligations is that they become legally liable for the mandatory, complete, and transparent disclosure of their entire global financial footprint. This involves a detailed reporting obligation of all Foreign Assets they hold anywhere outside India—ranging from bank accounts and immovable property to financial interests in entities—as well as reporting any Income generated from these sources outside India, directly within their Indian Income Tax Return (ITR) filings, typically under the specific "Schedule FA".

Requirement Disclosure of Foreign Assets In ITR

- As per the Indian tax laws, every ordinary tax resident individual owns any Foreign Assets like Bank Account, Foreign Shares, Foreign Mutual Funds, Immovable Property Outside India or any other Foreign Asset, then it is mandatory for such individual to fill the information in schedule FA while filing his ITR.

- If an individual has invested in any foreign assets (being shares or mutual funds in a foreign company, etc.) directly or holds stock options (ESOPs) of foreign companies, then it is mandatory for such individual to fill schedule FA of his ITR.

- An individual needs to file both schedule FA and schedule VDA (Virtual Digital Assets) where he has purchased VDAs from international exchanges and also storing them in foreign wallets.

What is The Black Money Act?

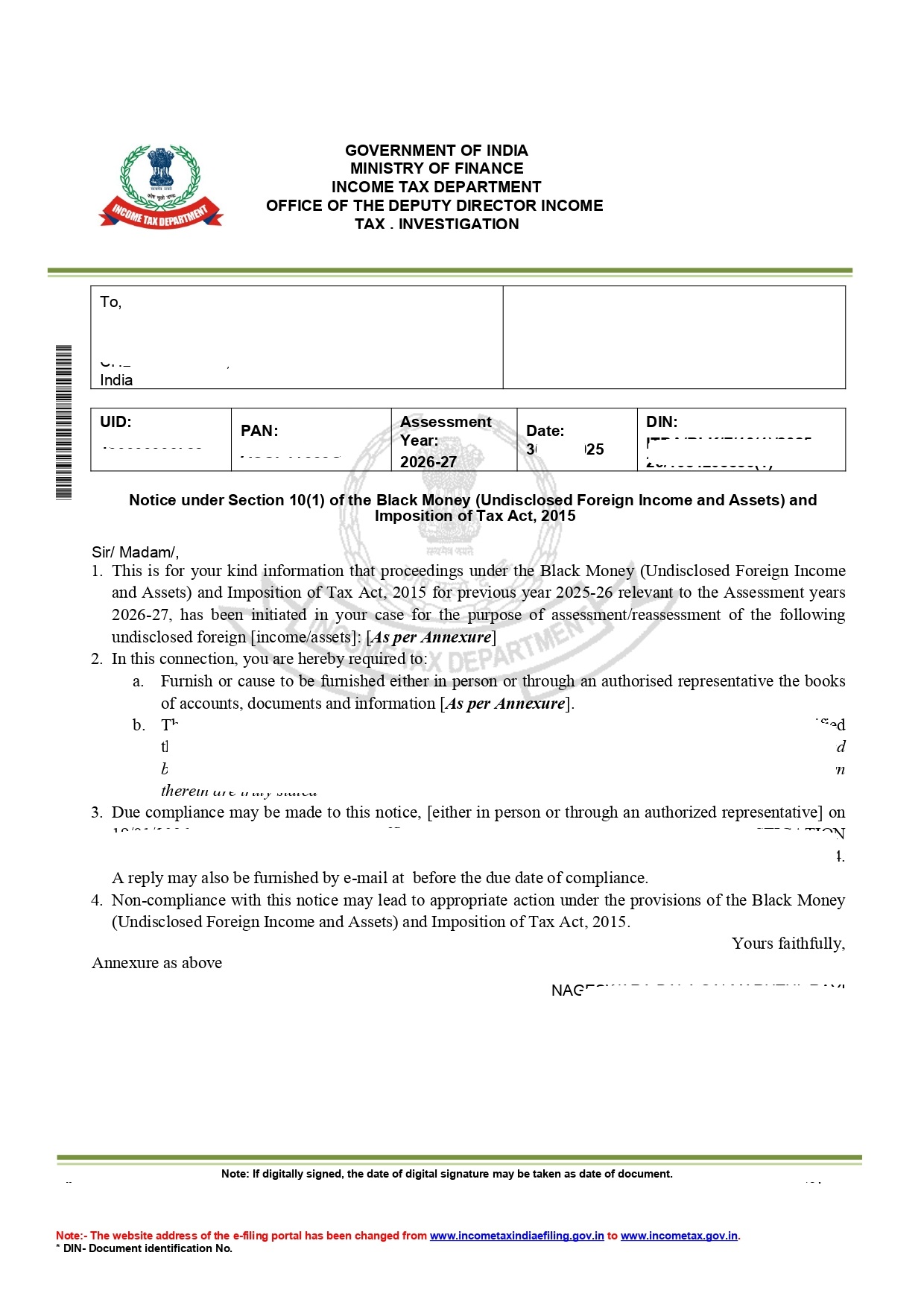

- Black Money Act full name is Black Money (Undisclosed Income and Assets) and Imposition of Tax Act, 2015. This Act has come into force in 2015. However, in recent 2-3 years, the tax authorities (Foreign Assets Investigation Unit ‘FAIU’), who are entrusted to investigate and implement the proceedings of Black Money Act, has started sending notices for non-compliances of this Act.

- Section 43 of Black Money Act provide for penalty for non-disclosure of foreign assets detail in ITR.

- Its provisions are applicable on Resident Individual i.e. Individual who is ordinary tax Resident of India.

- As per this provision, it is mandatory to provide information of foreign assets outside India while filing the ITR.

- Failure to disclose foreign assets in ITR – Straight penalty of Rs 10 Lacs per defaulting year i.e. the year in which the foreign assets were not reported in ITR. If non-disclosure is in more than one year, then Assessing Officer can levy penalty for each defaulting year.

- Further to above, section 3 of Black Money Act provides for levy of tax on undisclosed Income or Foreign Asset. It provides straight tax @30% on undisclosed Income or Foreign Asset.

- Further, as per section 41 of Black Money Act, if there is any taxes levied under this Act on undisclosed income or Foreign assets, then a penalty of three times of that tax shall be levied as penalty. Hence, if any amount is found undisclosed under this Act proceedings, then total of 120% (30% plus 3 times of that amount) of that amount is payable under this Act.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

The Severe Consequences of Non-Compliance: Enter the Black Money Act

The Importance of Proactive Understanding and Compliance

Therefore, given the incredibly high financial and legal stakes involved in this scenario, it is absolutely crucial and of paramount importance for all affected taxpayers to proactively gain a comprehensive and thorough understanding of the entire legal landscape surrounding this issue. This includes mastering the specific and often draconian provisions of the Black Money Act, fully grasping the detailed procedural requirements for accurate Foreign Assets and Income Disclosure in the ITR, and realizing the profound, potentially life-altering, and deeply burdensome tax implications these laws hold specifically for Returning NRIs and other newly designated Tax Residents in India.

Foreign Assets Investigation Unit (FAIU) – Proceedings To Investigate Foreign Assets Transactions

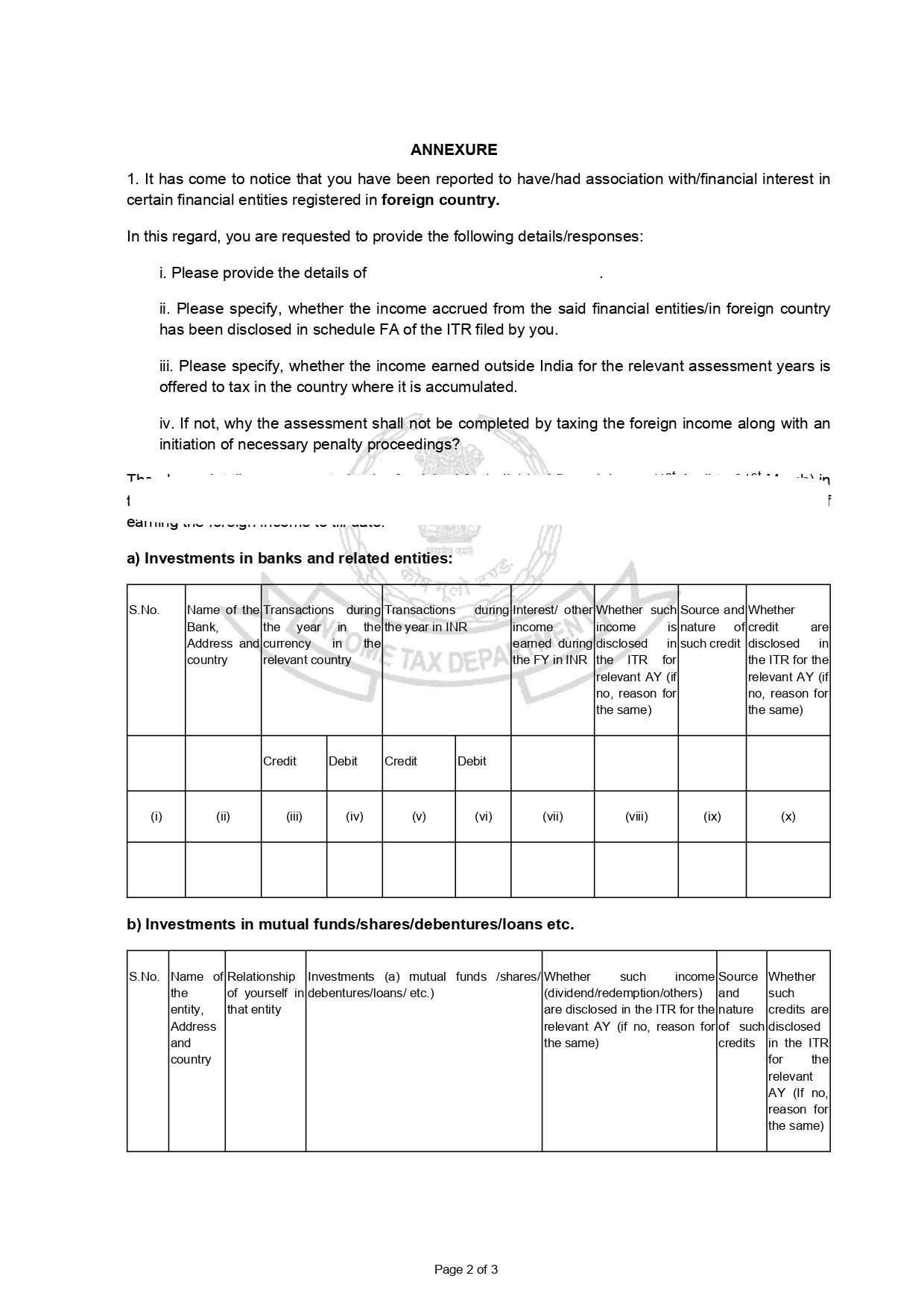

- Income Tax Department has set up a separate department in all major cities to investigate the Foreign Assets Transactions. It is named as Foreign Assets Investigation Unit (FAIU). It is headed by an officer of Deputy Director of Income Tax (DDIT).

- The FAIU Deptt receives data from various sources (including foreign country income tax department under the agreement with that country for information exchange).

- When this department has reasons to believe that Foreign Assets information is not disclosed or disclosed incompletely/inaccurately, the FAIU Office issues summon under section 131 of Income Tax Act to initiate the investigation to enquire it.

- On receipt of the information the FAIU office prepares a report and submit to its senior authorities and on their approval, FAIU finalizes its findings.

- Lot of NRIs/OCIs are also receiving notices u/s 131. Reason for this is, FAIU gets foreign assets information however there is no ITR filed by these NRIs/OCIs, which gives reason to FAIU office to initiate an enquiry. Hence, for NRIs/OCIs, ITR filing is helpful to avoid this summon or other type of notices.

- If there are negative findings then proceedings of Black Money (Undisclosed Income and Assets) and Imposition of Tax Act, 2015 are initiated by this office to levy & collect penalty and taxes.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Landmark Case - Shobha Harish Thawani v. JCIT

Facts of the case

Assessee had declared interest income from foreign investment in AY 2016-17 and when this asset was sold, the capital gain was also offered to tax in AY 2019-20. However, the Assessee failed to disclose this foreign asset in schedule FA while filing the ITR for AY 2016-17 to 2018-19.

Accordingly, the Assessing Officer (AO), under the Black Money Act 2015, levied a penalty towards this non-disclosure. On appeal, the CIT(A) upheld this levying of penalty. The aggrieved then filed an appeal before the Tribunal.

ITAT Held

- Section 43 of Black Money Act, 2015, levies penalty for failure to furnish information or furnishing inaccurate information about a foreign asset in the ITR.

- Section applicable on Resident or Ordinarily Resident Person

- The said disclosure is to be made in schedule FA of the relevant ITR

- Foreign asset includes any asset held by the Assessee as a beneficial owner or otherwise

- Since the Assessee failed to disclosed foreign asset in schedule FA of ITR, hence this penalty was rightly levied.

- Then the Assessee contented that the word used in the section is that the ‘AO “may” levy penalty’, accordingly this penalty is not mandatory but is at the discretion of the AO.

- It was held that the Assessee failed to substantiate that the AO has extravagantly exercised his discretion and that the AO levied penalty judiciously after duly examining the facts of the case. Further, there was no evidence to prove the penalty arbitrary and unjustified.

- Provisions of Section 43 provides for levy of penalty in case of non-disclosure of foreign assets in schedule FA and accordingly, does not leave any scope for not levying penalty even if foreign asset is disclosed in books

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Frequent Asked Questions (FAQs) on Foreign Asset Disclosures, Black Money Act, Tax Implications on Returning NRIs/Foreign Citizens

An Individual, who is Resident in India and an Ordinary Resident, is required to file foreign assets detail in the FA Schedule of ITR form. This is not mandatory for NRIs or OCIs who are living & working abroad, and who are Non-resident in India as per Indian tax laws. However, those NRIs/OCIs, who return back to India and becomes Ordinary Resident in India, are required to submit foreign asset details in their ITR form.

A returning NRIs/OCIs may maintain his status as Not Ordinary Resident for 2-3 years after returning back to India. To the extent he/she is Non-resident or Not Ordinary Resident, there is no requirement of submitting Foreign Asset details. Hence, ITR is also not mandatory. Once he/she becomes an Ordinary Resident, their Foreign Assets as well Foreign Income will also be incorporated in the Indian ITR. Hence, ITR filing is mandatory in that case. Also, it is important to understand that for a continuous track record as well avoiding various Income tax automated enquiries, ITR filing is important and beneficial.

Though provisions of foreign asset disclosures are not applicable to NRIs/OCIs living abroad. However, Inc Tax Deptt (FAIU) gets information from the tax offices of foreign countries (under mutual information exchange clause of Tax Agreements between countries) and also some other sources. Hence, when there is no ITR filied by these NRIs/OCIs, then to confirm a non-compliance, FAIU issues notice to NRIs/OCIs also. Hence, it is advisable for NRIs/OCIs that they file ITR in India to submit their non-resident status with the Tax Department.

If an individual has a foreign bank account(s) and balance in aggregate of all said foreign bank account(s) does not exceed Rs 5 Lakh, then penalty under section 43 of the Black Money Act cannot be imposed even if such bank account was not declared in schedule FA.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

Detailed Real Life scenario of an NRI Client Regarding Foreign Asset Disclosure Notices

Background: The individual held the legal status of a Non-Resident Indian (NRI) for tax purposes. Approximately four years prior to this date, they permanently relocated from their previous residence in Bangalore, India, and moved to Australia for the primary purpose of pursuing long-term employment opportunities. In the recent past, this individual was in receipt of an official electronic communication via email originating directly from the Income Tax Department of India, specifically concerning the bank accounts that they currently maintain in Australia. Through

Question Posed by the Client: Given my current situation and status, am I legally obligated under Indian tax laws to report my foreign bank account held in Australia, along with any other international assets and foreign-sourced income, when filing my Indian Income Tax Return (ITR)?

Answer: Understanding Applicability Based on Residential Status

The Legal Requirement Under the Black Money Act - According to the stringent stipulations laid down in Indian prevailing laws—specifically referencing the stringent provisions of the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015—there exists a mandatory statutory requirement for taxpayers to fully disclose and report all their foreign assets situated outside India (such as bank accounts, property, and investments), as well as any foreign income derived from sources outside India, directly within their Indian Income Tax Return (ITR) filings under the dedicated "Schedule FA".

Scope of Applicability: Resident and Ordinary Resident (ROR) It is absolutely crucial to note, however, that the applicability of this specific draconian law regarding mandatory global asset disclosure is strictly limited and targeted only towards individuals whose residential status for the relevant financial year is categorized under the Income Tax Act as "Resident and Ordinary Resident" (ROR) in India.

Exclusions: Non-Residents and NORs Conversely, these stringent disclosure provisions and the subsequent penalties under the Black Money Act for non-disclosure do not extend their applicability to individuals who fall under the tax categories of Non-Residents (NR) or individuals classified as Resident but "Not Ordinary Residents" (NOR) during the relevant financial year.

Conclusion for the NRI Clients - Therefore, based on the facts presented where you have stated you are currently classified as a Non-Resident (NR) in India for tax purposes following your move to Australia four years ago, you are not legally required to report or disclose details of your Australian bank account or other foreign assets and overseas income in your Indian Income Tax Return filings.

Crucial Compliance Warning Notwithstanding this specific exemption from reporting foreign assets due to your NRI status, it is of paramount importance that you exercise extreme caution and ensure due diligence while preparing your tax documents, guaranteeing that you are selecting and filing the appropriate ITR form that accurately reflects and explicitly declares your correct residential status as a Non-Resident to avoid any future scrutiny or mismatch notices from the tax department.

CA Mitesh and Associates is India's leading CA Firm Firm with special focus on accurate Income Tax Return filing and Handling Income Tax Notices in India. Contact us via WhatsApp: Click Here or Email: info@mnpartners.in

DISCLAIMER

CMS Meta

- Non-Disclosure of Foreign Assets ITR

Black Money Act India NRIs

Returning NRI Tax Implications India

Foreign Asset Disclosure Rules India

Schedule FA Income Tax Return

Tax Resident Status for Returning NRIs

OCI foreign asset reporting requirements

Comments