What to do when you receive Notice u/s 148?

In this post we will discuss all aspects about What to do when you receive Notice u/s 148 in India? This is a long article so buckle up.

Table of Contents

- Explanation of Notice u/s 148

- Importance of responding to the notice u/s 148

- How is it different from other notices?

- Reasons for receiving notice u/s 148

- Time limit for issuing notice u/s 148

- Verification of the notice

- Consequences of an invalid notice

- Options for responding to the notice

- Documents required for responding to the notice

- Benefits of hiring a professional

- What are the different types of hearings under section 148?

- Procedure to follow during hearings

- Negotiate with the tax authorities

- Procedure to be followed during negotiation

- Conclusion

Explanation of Notice u/s 148

An income tax notice under section 148 of the Income Tax Act is a notice issued by the income tax department to taxpayers if the department has reason to believe that the taxpayer has undisclosed income that has escaped taxation. This section allows the tax department to reopen an assessment that has already been completed if they have reason to believe that income has been under-reported or not disclosed.

The notice under section 148 is usually issued within four years from the end of the relevant assessment year. However, in certain cases, such as where income over Rs. 1 lakh has escaped assessment, the notice can be issued up to six years from the end of the relevant assessment year. In certain circumstances, such as in cases involving income from assets located outside India, the notice can be issued up to sixteen years from the end of the relevant assessment year.

If a taxpayer receives a notice under section 148, it is important to respond to it within the specified time frame and provide all necessary information and documents to the tax department. Failure to respond to the notice or provide the required information can result in penalties and further legal action by the tax department.

Importance of responding to the notice u/s 148

Avoiding penalties: Failure to respond to the notice or provide the necessary information and documents can result in penalties being imposed by the income tax department.

Legal obligations: As a taxpayer, it is your legal obligation to comply with the income tax laws of the country. Failing to respond to a notice can lead to further legal action against you.

Protection of rights: Responding to the notice allows you to exercise your legal rights as a taxpayer, such as the right to appeal against an assessment made by the income tax department.

Resolution of issues: By responding to the notice and providing the necessary information and documents, you can help resolve any issues or discrepancies that may have led to the notice being issued.

So responding to an income tax notice issued under section 148 is important for complying with the law, avoiding penalties, protecting your rights as a taxpayer, and resolving any issues with the tax department.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

How is it different from other notices?

An income tax notice issued under section 148 is different from other notices in terms of its purpose, timeframe, scope, and legal implications. It is important for taxpayers to understand the differences and respond appropriately to each notice they receive from the income tax department.

Purpose: The primary purpose of an income tax notice issued under section 148 is to inform the taxpayer that the income tax department has reason to believe that the taxpayer has undisclosed income that has escaped taxation. Other notices may be issued for different purposes, such as seeking clarification on a tax return filed by the taxpayer or requesting the taxpayer to provide additional information.

Timeframe: The timeframe for responding to an income tax notice issued under section 148 is generally shorter than other notices. The taxpayer is usually required to respond within a specific timeframe, failing which penalties may be imposed.

Scope: An income tax notice issued under section 148 can result in a reassessment of the taxpayer's income for a specific assessment year. Other notices may not have such a broad scope and may be limited to specific aspects of the taxpayer's income or tax return.

Legal implications: An income tax notice issued under section 148 has significant legal implications, as it can result in penalties and further legal action by the income tax department. Other notices may have different legal implications depending on their purpose and scope.

Reasons for receiving notice u/s 148

Failure to file tax returns: If a taxpayer has not filed their income tax return or has filed an incomplete or inaccurate return, the income tax department may issue a notice under section 148.

Under-reporting of income: If the income tax department has reason to believe that a taxpayer has under-reported their income or has undisclosed income, they may issue a notice under section 148.

Misreporting of income: If the income tax department has reason to believe that a taxpayer has intentionally misreported their income or has provided inaccurate information in their tax return, they may issue a notice under section 148.

Overlooked income: If the income tax department has reason to believe that a taxpayer has overlooked or failed to report certain income, such as income from investments or rental income, they may issue a notice under section 148.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

Time limit for issuing notice u/s 148

However, in certain cases, such as when income has escaped assessment or been under-reported, the income tax department may issue a notice under section 148 up to six years from the end of the relevant assessment year. In such cases, the income tax department must have reason to believe that income has escaped assessment amounting to Rs. 1 lakh or more in the relevant assessment year.

In certain exceptional cases, such as when income from assets located outside India has escaped assessment, the income tax department may issue a notice under section 148 up to sixteen years from the end of the relevant assessment year.

It is important for taxpayers to respond to any notice issued under section 148 within the specified time limit and provide all necessary information and documents to the income tax department. Failure to respond to the notice or provide the required information can result in penalties and further legal action by the income tax department.

Verification of the notice

It is important for taxpayers to verify the authenticity of any notice they receive from the income tax department, including a notice issued under section 148. Here are some steps that taxpayers can take to verify the notice:

Check the PAN and address: The notice should have the correct Permanent Account Number (PAN) and address of the taxpayer. If there are any discrepancies, it could be a sign that the notice is not genuine.

Check the communication channel: The notice should be sent through an official communication channel, such as registered post or email from the income tax department's official email ID. If the notice is sent through an unofficial channel or from a suspicious email ID, it could be a sign that the notice is not genuine.

Verify the signature: The notice should be signed by an authorized officer of the income tax department. Taxpayers can verify the signature by checking it against the list of authorized officers on the income tax department's website.

Contact the income tax department: If taxpayers have any doubts about the authenticity of the notice, they can contact the income tax department's customer service helpline or visit the nearest income tax office to verify the notice.

Consequences of an invalid notice

If a taxpayer receives an invalid notice, such as a notice issued without proper authorization or for a time period beyond the statutory time limit, they are not legally obligated to respond to it. However, if the taxpayer fails to respond to a valid notice issued under section 148, they could face penalties and further legal action by the income tax department.

Failure to respond to a valid notice can lead to the income tax department treating the taxpayer as a defaulter, and can result in the imposition of penalties, interest, and fines. The income tax department may also initiate legal proceedings against the taxpayer, which could result in court appearances and other legal complications.

Options for responding to the notice

When a taxpayer receives a notice under section 148 of the Income Tax Act, they have several options for responding to the notice. Here are some of them:

File a return: If the taxpayer has not filed their income tax return for the relevant assessment year, they can file the return within the time limit mentioned in the notice. Once the return is filed, the income tax department will consider it as a response to the notice.

Seek clarification: The taxpayer can seek clarification from the income tax department about the reason for issuing the notice and the information and documents required to respond to the notice.

Provide information: The taxpayer can provide the information and documents required by the income tax department within the specified time limit mentioned in the notice.

Contest the notice: If the taxpayer disagrees with the reasons mentioned in the notice, they can contest the notice by filing a reply explaining their position and providing supporting documents.

Seek professional help: If the taxpayer is not confident about responding to the notice on their own, they can seek help from a tax professional or a chartered accountant who can assist them in preparing a proper response to the notice.

Documents required for responding to the notice

The documents required for responding to a notice under section 148 of the Income Tax Act may vary depending on the reason for issuing the notice. However, here are some of the common documents that taxpayers may need to provide:

Copy of the original return: If the notice is related to a discrepancy in the taxpayer's original return, they may be required to provide a copy of the original return.

Bank statements: The taxpayer may be required to provide bank statements for the relevant financial year to support their income and expenses.

Salary and income statements: If the taxpayer is a salaried employee, they may be required to provide salary and income statements for the relevant financial year.

Investment documents: If the taxpayer has made any investments, such as in shares, mutual funds, or property, they may be required to provide investment documents to support their income and expenses.

Purchase and sale invoices: If the taxpayer is engaged in a business or profession, they may be required to provide purchase and sale invoices to support their income and expenses.

Loan documents: If the taxpayer has taken any loans, they may be required to provide loan documents to support their income and expenses.

Any other relevant documents: The income tax department may request any other relevant documents depending on the reason for issuing the notice.

For any help, assistance or feedback you may seek a consultation here - Appointment with CA. Please note the all consultations with the CA are Paid consultations.

Types of professionals to be consulted

Depending upon the notice details under section 148 of the Income Tax Act, taxpayer may need to consult with different professionals to ensure that they are meeting all the legal requirements and responding appropriately. Here are some of professionals that taxpayers may need to consult:

Chartered Accountant (CA): A CA is a professional who is trained in accounting, taxation, and financial management. A CA can help taxpayers to understand the notice, analyze their financial records, and respond to the notice in a timely and appropriate manner.

Tax Lawyer: A tax lawyer is a legal professional who specializes in tax law. They can provide legal advice to taxpayers on their rights and obligations under the Income Tax Act and represent them in legal proceedings if required.

- GST Practitioner: If the taxpayer is registered under the Goods and Services Tax (GST), they may need to consult a GST practitioner to ensure compliance with the GST provisions.

Company Secretary: If the taxpayer is a company, they may need to consult a company secretary to ensure compliance with the Companies Act and other applicable laws.

It is important for taxpayers to choose the right professionals to help them respond to the notice under section 148 of the Income Tax Act. They should choose professionals with the necessary skills, knowledge, and experience to provide the required advice and assistance.

Benefits of hiring a professional

Hiring a professional, such as a Chartered Accountant (CA), tax lawyer, etc, can offer several benefits when responding to a notice under section 148 of the Income Tax Act. Here are some of the benefits of hiring a professional:

Expert advice: Professionals have expertise and experience in handling tax-related matters. They can provide expert advice on the notice, analyze the taxpayer's financial records, and suggest the best course of action to take.

Compliance: Professionals can help taxpayers to ensure compliance with the provisions of the Income Tax Act. They can help taxpayers to avoid mistakes and errors that could lead to legal action or penalties.

Time-saving: Hiring a professional can save taxpayers time and effort in responding to the notice. The professional can handle the process of gathering documents, analyzing them, and preparing a response, allowing the taxpayer to focus on their business or other activities.

Legal representation: If legal action is required, such as an appeal to the Income Tax Appellate Tribunal (ITAT) or higher courts, a tax lawyer can represent the taxpayer in legal proceedings.

Confidentiality: Professionals are bound by ethical and legal obligations to maintain confidentiality. They can ensure that the taxpayer's financial information is kept confidential and secure.

Better financial planning: Professionals can help taxpayers to plan their finances in a way that minimizes their tax liability and maximizes their financial growth. They can provide advice on investment strategies, financial planning, and tax planning.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

Compliance: Attending hearings shows that the taxpayer is willing to comply with the requirements of the Income Tax Act. It demonstrates that the taxpayer is taking the matter seriously and is willing to cooperate with the authorities.

Understanding: Attending hearings allows the taxpayer to understand the nature of the notice and the concerns of the Income Tax Department. It provides an opportunity for the taxpayer to ask questions and seek clarifications.

Presentation of Evidence: Attending hearings provides an opportunity for the taxpayer to present evidence in support of their case. The taxpayer can explain their position and provide evidence to back it up.

Negotiation: Attending hearings allows for negotiation between the taxpayer and the Income Tax Department. The taxpayer can negotiate a settlement or a mutually agreeable resolution.

Avoidance of Penalties: Attending hearings can help the taxpayer to avoid penalties. If the taxpayer is able to provide a satisfactory explanation or evidence, the Income Tax Department may waive penalties or reduce them.

Legal representation: Attending hearings allows the taxpayer to be represented by legal counsel. A tax lawyer can represent the taxpayer in legal proceedings, present evidence, and negotiate with the Income Tax Department on their behalf.

What are the different types of hearings under section 148?

When responding to a notice under section 148 of the Income Tax Act, there may be different types of hearings that a taxpayer need to be aware of:

Personal Hearing: A personal hearing is a meeting between the taxpayer and the Income Tax Officer (ITO) where the taxpayer can provide evidence and clarification in person. The taxpayer may be asked to attend a personal hearing to provide additional information or explanation.

Assessment Hearing: An assessment hearing is a hearing before the Assessing Officer (AO) where the taxpayer can present evidence and explain their position on any issues raised in the notice. The AO will assess the taxpayer's return of income and may make adjustments or additions based on the evidence presented.

Appellate Hearing: If the taxpayer disagrees with the assessment made by the AO, they can file an appeal with the Commissioner of Income Tax (Appeals) [CIT(A)]. The taxpayer may be required to attend an appellate hearing where they can present their case and provide evidence in support of their position.

Penalty Hearing: If the Income Tax Department decides to impose a penalty, the taxpayer may be required to attend a penalty hearing to explain their position and provide evidence in support of any mitigating factors.

Prosecution Hearing: In cases where the taxpayer is suspected of tax evasion or other tax-related offences, a prosecution hearing may be held. The taxpayer may be required to attend a prosecution hearing where they can provide evidence and defend themselves against the charges.

Procedure to follow during hearings

When attending a hearing in response to a notice under section 148 of the Income Tax Act, it is important to follow certain procedures to ensure that the process runs smoothly. Here are some of the procedures that should be followed during a hearing:

Be on time: Ensure that you arrive on time for the hearing. Being late may result in the hearing being adjourned or delayed.

Be prepared: Ensure that you are prepared for the hearing. Bring all necessary documents and evidence to support your case.

Be respectful: Be respectful to the authorities and other parties involved in the hearing. Maintain a professional demeanor and avoid getting emotional or argumentative.

Answer truthfully: Answer all questions truthfully and to the best of your knowledge. Do not provide false or misleading information.

Stay on topic: Focus on the issues raised in the notice and avoid discussing irrelevant matters.

Listen carefully: Listen carefully to the questions asked and the concerns raised by the authorities. Take notes if necessary.

Provide evidence: Provide evidence to support your position. Make sure that the evidence is relevant, admissible, and properly documented.

Ask for clarification: If you do not understand a question or need clarification, ask for it.

Take breaks if needed: If the hearing is long or if you need a break, ask for one.

Follow up: After the hearing, follow up with the authorities to ensure that the next steps are clear and understood.

Negotiate with the tax authorities

Payment plan: A payment plan allows you to pay off your tax debt over time. You can negotiate a payment plan with the tax authorities, where you agree to make regular payments towards the tax debt until it is paid off in full.

Settlement offer: A settlement offer allows you to settle your tax debt for less than the full amount owed. You can negotiate a settlement offer with the tax authorities, where you agree to pay a lump sum to settle the tax debt in full.

Penalty abatement: Penalty abatement allows you to reduce or eliminate any penalties or interest that have been assessed on your tax debt. You can negotiate penalty abatement with the tax authorities by demonstrating that you had a reasonable cause for your failure to pay your taxes on time.

Offer in compromise: An offer in compromise allows you to settle your tax debt for less than the full amount owed, based on your ability to pay. You can negotiate an offer in compromise with the tax authorities by demonstrating that you are unable to pay the full amount of your tax debt.

Innocent spouse relief: Innocent spouse relief allows you to avoid paying any tax liabilities that arise from your spouse's tax returns. You can negotiate innocent spouse relief with the tax authorities by demonstrating that you were unaware of any errors or omissions on your spouse's tax returns.

Have you received any income tax notices? Trust us to assist you in responding to the IT Department. Our team at CA Mitesh & Associates is well-versed in engaging with the Income Tax Department. By assisting you in responding properly, our team will help you avoid legal repercussions & penalties.

Procedure to be followed during negotiation

Gather all relevant information: Collect all relevant financial and tax-related documents that are needed for the negotiation process. These documents can include income tax returns, bank statements, financial statements, and any other documents that relate to your tax liability.

Analyze the notice and identify the issues: Review the notice to understand the reason for the tax liability and identify the specific issues that need to be addressed during the negotiation process.

Develop a negotiation strategy: Based on the issues identified, develop a negotiation strategy that outlines the goals of the negotiation, the arguments to be presented, and any potential settlement options.

Initiate contact with the tax authorities: Initiate contact with the tax authorities to schedule a meeting or to communicate through written correspondence. During this communication, clearly present your negotiation strategy and explain your position.

Present your case: During the negotiation, present your case in a clear and concise manner. Use the information gathered and the negotiation strategy developed to support your position.

Consider settlement options: If the tax authorities propose a settlement offer, consider the terms of the offer carefully. Determine if the proposed settlement is acceptable and whether it aligns with the goals of the negotiation.

Finalize the agreement: Once an agreement has been reached, finalize the terms of the agreement in writing. Ensure that all parties involved understand and agree to the terms of the agreement.

Conclusion

In conclusion, receiving a notice u/s 148 can be a daunting task for taxpayers. However, it is important to understand the notice and respond to it in a timely and efficient manner. By following the points discussed in this article, taxpayers can effectively respond to the notice u/s 148 and avoid any penalties or legal action. Remember, maintaining proper tax compliance and staying informed can go a long way in ensuring a hassle-free tax experience.

For any help, assistance or feedback you may seek a consultation here - Appointment with CA.

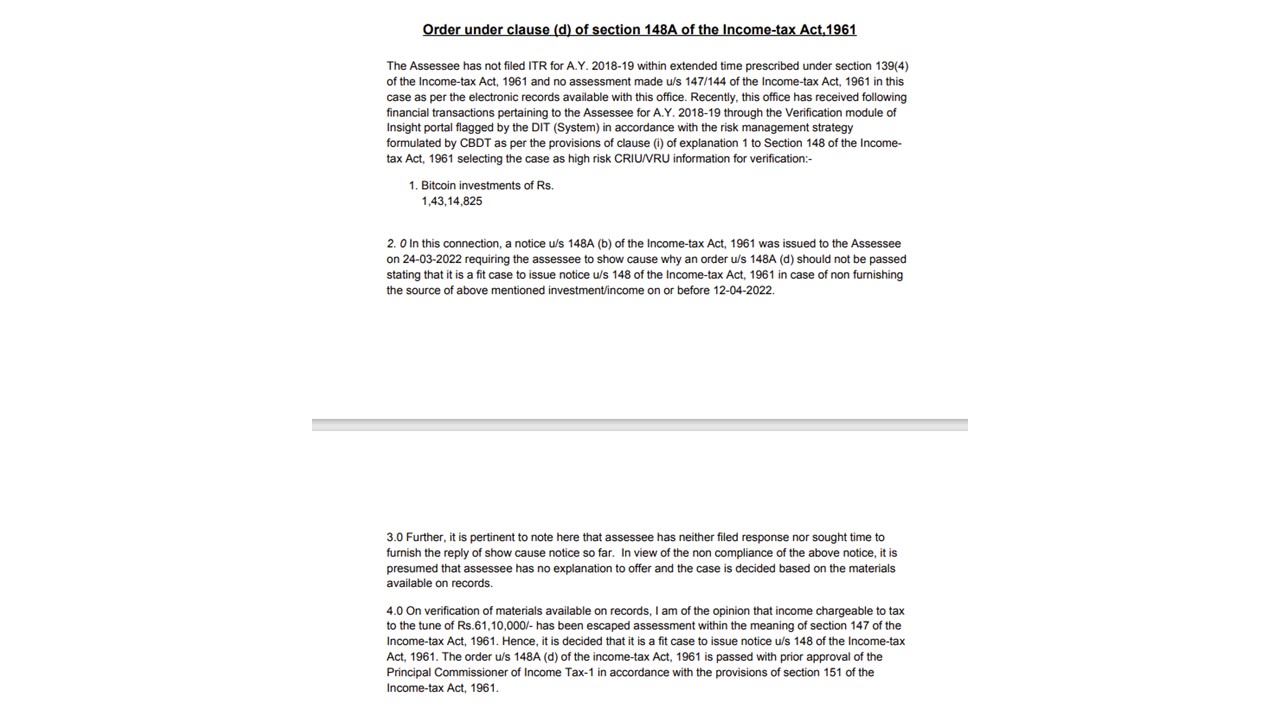

Free Examples of Notice u/s 148 received by our Clients

DISCLAIMER

Comments