Favourable Order against Income Tax Notice for trading in Cryptocurrency

We are very happy that we were able to get a favourable order against Income Tax Notice which was served on our client. The case involved huge assessment order passed by the income tax department against the client for trading in cryptocurrency namely Bitcoins in FY 2017-18.

Table of Contents

CA Mitesh and Associates is India's leading CA Firm for Managing and Responding to Income Tax Notices with special focus on Crypto matters and NRI Investments in India. Check out details of our Managing and Responding to Income Tax Notices

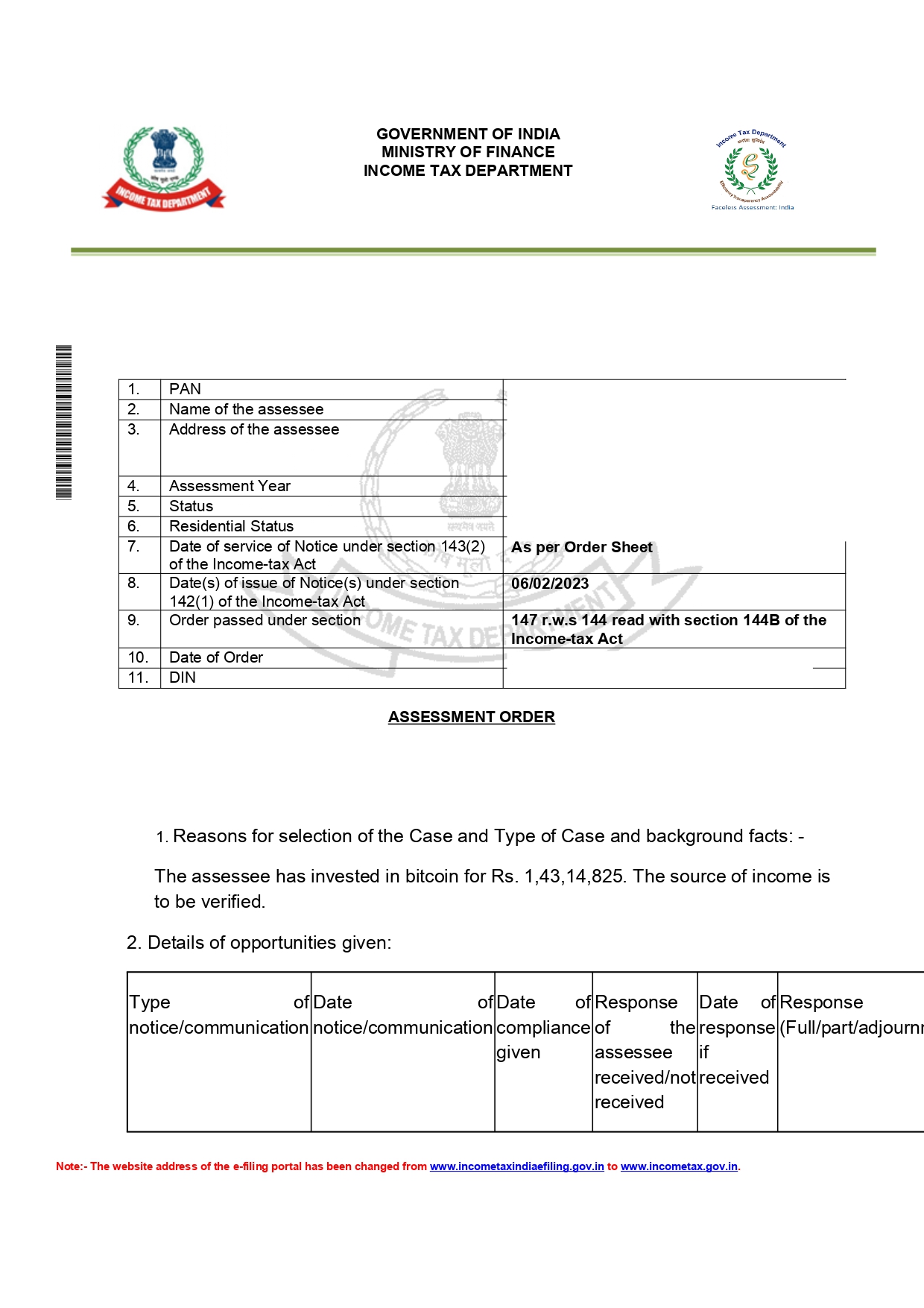

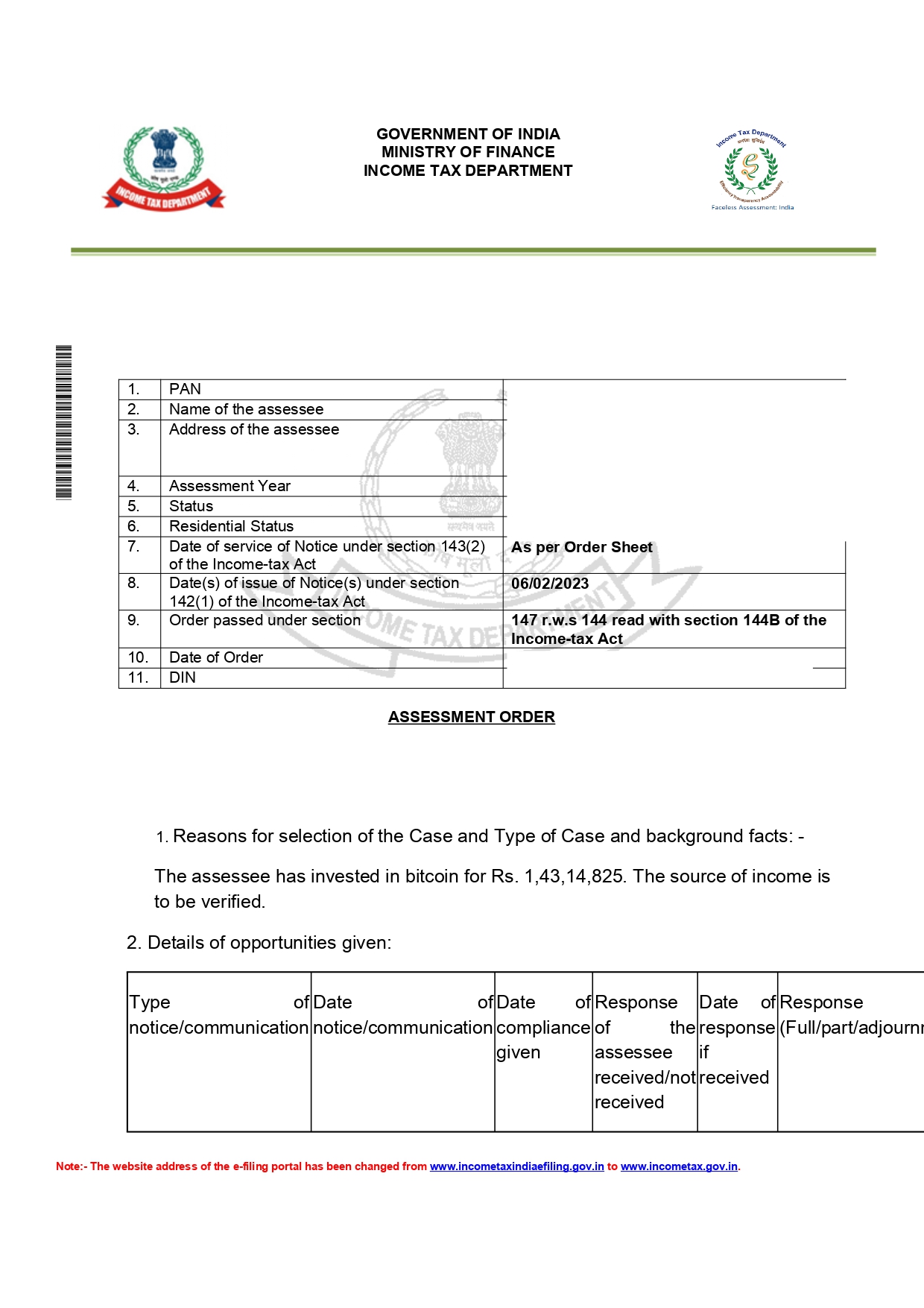

Case Background

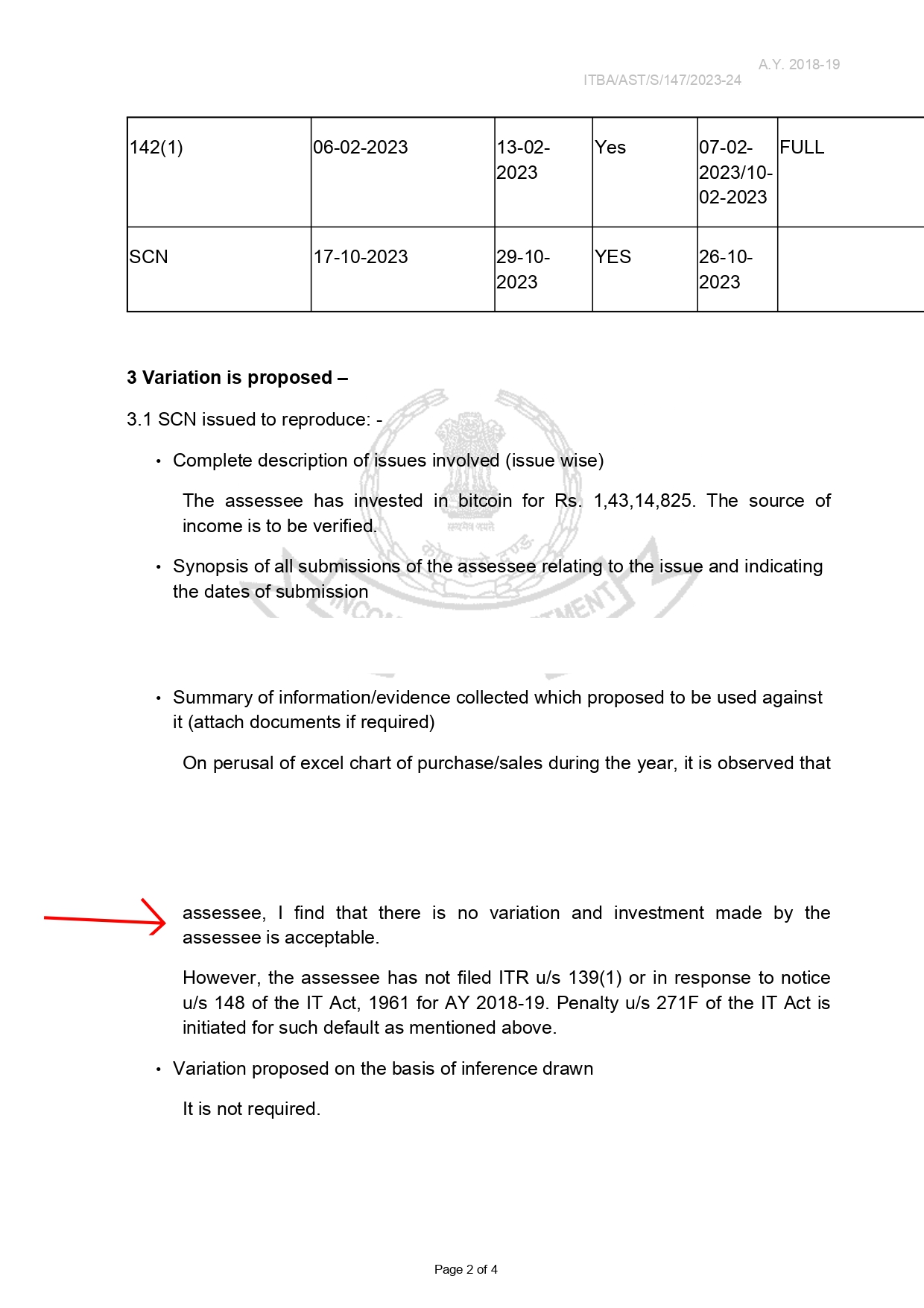

Notice Received by Client under section 148A which stated as follows -

"Whereas I have information which suggests that income chargeable to tax for the Assessment Year 2018-19 has escaped assessment within the meaning of section 147 of the Income-tax Act, 1961. The details of the information/ enquiry conducted on which reliance is being placed, along with supporting documents, are enclosed with this notice.

You are required to show-cause as to why, in view of the details contained in enclosures mentioned in point number 1 above, a notice section 148 of the Income tax Act, 1961 should not be issued.

You may submit your reply to this notice, along with supporting documents (if any) on the above mentioned issues on or before xx-xx-xxxx."

In this connection Notice u/s. 148A was issued on xx/xx/xxxx to our client and asked him to furnish the following information:

- Details of Bitcoins purchased during the Y. 2017-18.

- Details of Bitcoins sold during the Y. 2017-18.

- Details of capital gain/profit on Bitcoins sold during the Y. 2017-18.

- Details of cost of acquisition for the bitcoins sold during the Y. 2017-18.

- Sources for the Bitcoins purchased during the Y. 2017-18 with supporting documentary evidence.

- Certified ledger account copy of your account in the books of Secure Bitcoin Traders Pvt Ltd for Y. 2017-18.

- Certified ledger account copy of your account in the books of M/s Skysharp IT Solutions Pvt ltd for Y. 2017-18.

- Documentary evidence for the claim of cost of acquisition for the bitcoins sold during the Y. 2017-18.

- Date, Mode of payment of sale consideration for purchase of Bitcoins, please furnish the relevant bank account statements highlighting the transactions with sources for purchase of the bitcoins.

- Details of all the bank accounts held during the financial year 2017-18.

- Copy of Credit Card statement for the relevant year along with sources for credit card

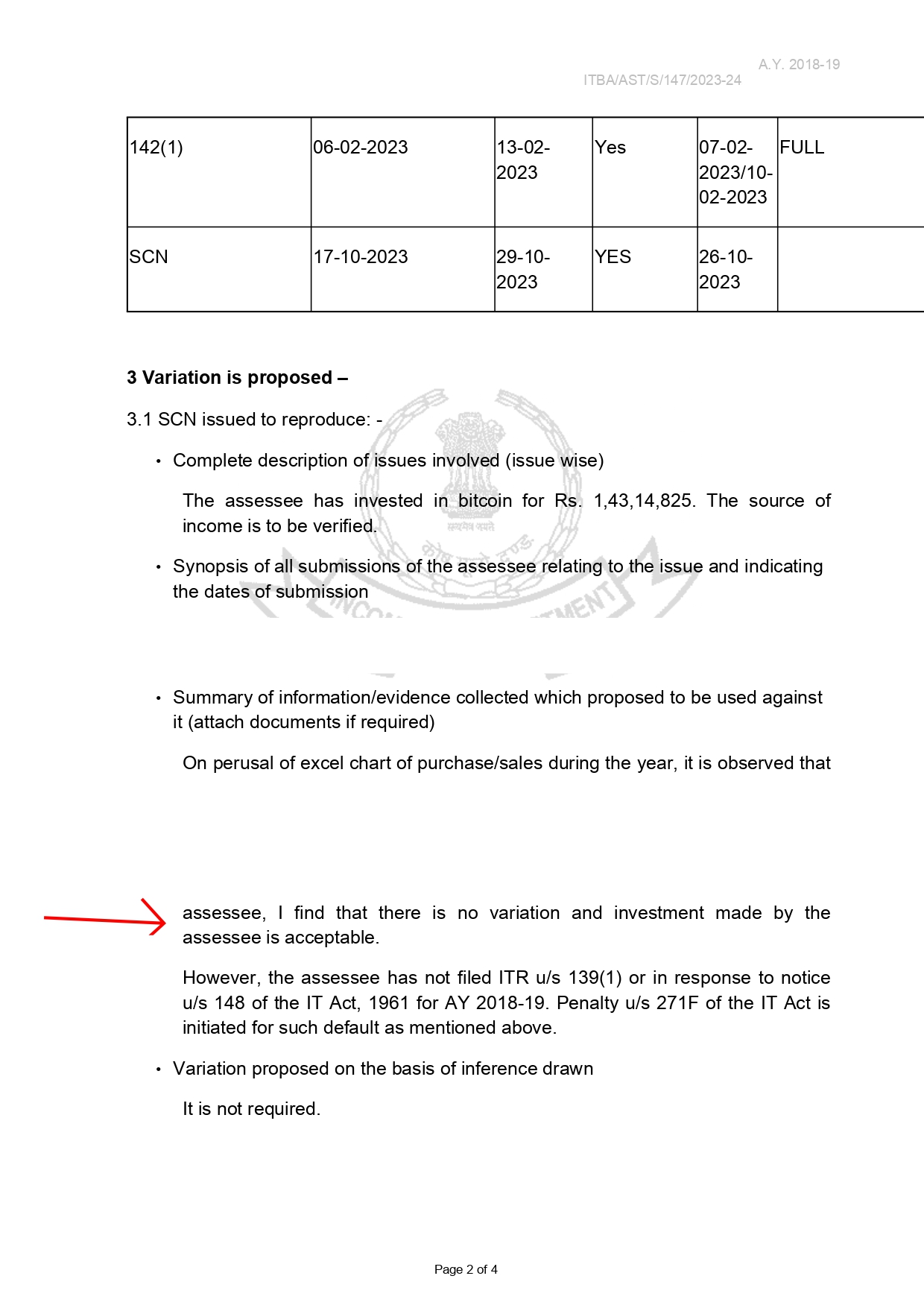

Income Tax Department alleged that "It is seen that in spite of indulging in the Huge Bitcoin Trading transactions, in assessee’s ITR for 2018-19, the assessee has not disclosed the transactions in the ITR filed."

It further alleged that "It may also be noted that in case of no response on or before the date mentioned in the notice, it would be considered that you have no submissions to make and the undersigned will be constrained to proceed with the proceedings as per the provisions of section 148A of the Act, on the basis of the documents/information available on record."

Our Responses

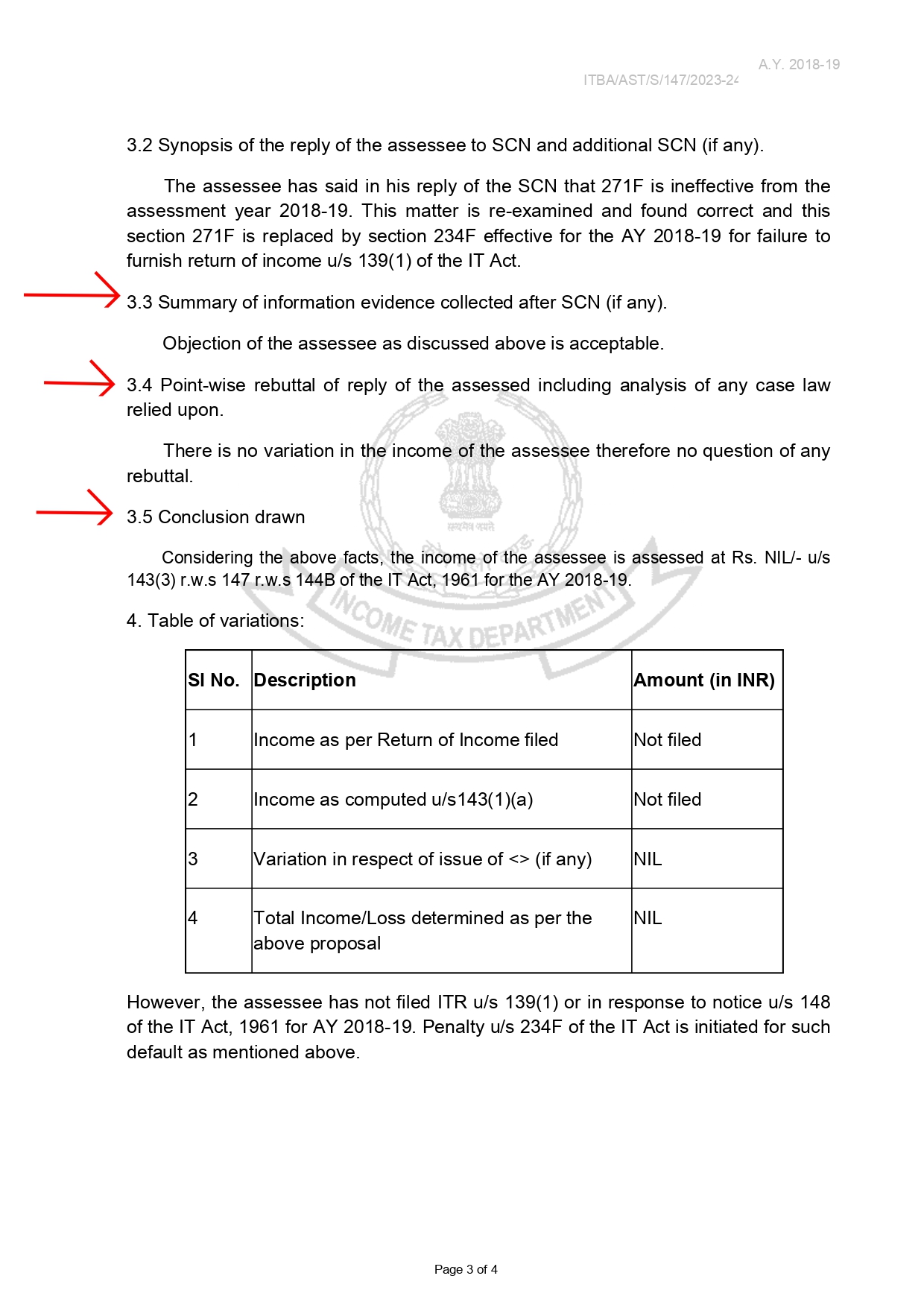

We submitted a response on behalf of the client, providing copies of bank statements and all other available evidence in response to the notice. Additionally, we obtained details from Coinsecure (also known as M/s Skysharp IT Solutions Pvt Ltd and Secure Bitcoin Traders Pvt Ltd) regarding the trades conducted by our client during the fiscal year 2017-18. The department raised further queries regarding our response, which were promptly addressed and clarified.

Conclusion

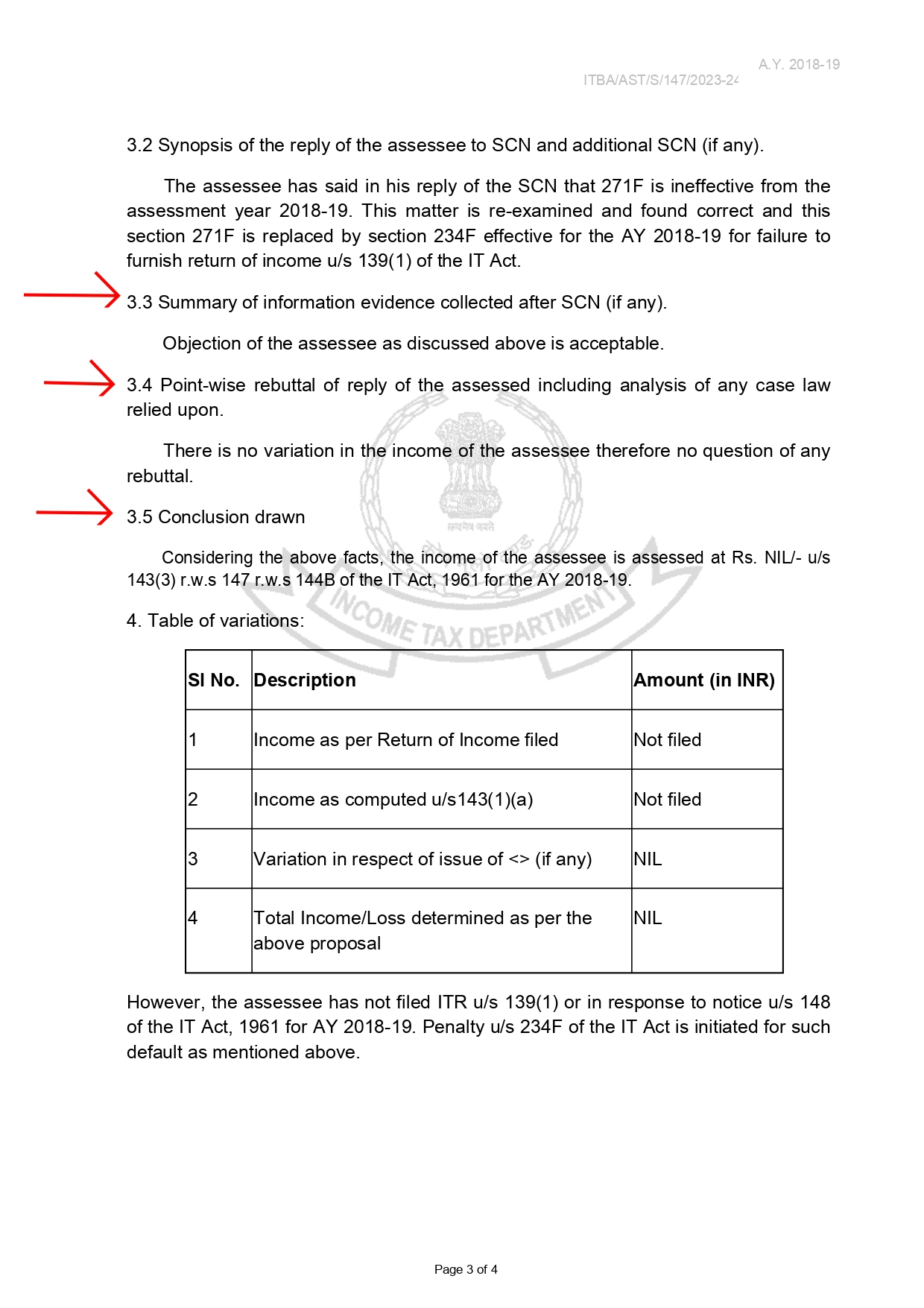

Department agreed with our response and issued the following order

Considering the facts submitted, the income of the assessee is assessed at Rs. NIL/- u/s 143(3) r.w.s 147 r.w.s 144B of the IT Act, 1961 for the AY 2018-19

| Sl No. | Description | Amount (in INR) |

| 1 | Income as per Return of Income filed | Not filed |

| 2 | Income as computed u/s143(1)(a) | Not filed |

| 3 | Variation in respect of issue of <> (if any) | NIL |

| 4 | Total Income/Loss determined as per the above proposal | NIL |

However, the assessee has not filed ITR u/s 139(1) or in response to notice u/s 148

of the IT Act, 1961 for AY 2018-19. Penalty u/s 234F of the IT Act is initiated for such

default as mentioned above.

Because the Income Tax Return was not filed by the assessee the department did levy a penalty u/s 234F.

Comments